When the venue turns into a part of the product, which file is authoritative?

When SpaceX listed on Nasdaq as SPCX in June 2026, crypto customers met a number of variations without delay: Binance Pockets SPCXx, Bybit IPO Categorical, Backpack SPCX on Solana, and SPCXUSDT pre-IPO perps. The names had been comparable, however the merchandise created totally different claims and information.

RWA venues don’t commerce one asset file. They commerce claims whose authority sits in several file programs.

The break occurred on the allocation layer. Crypto venues might gather subscriptions, lock USDC, and outline refund phrases. They didn’t management whether or not the upstream supplier acquired shares or might ship the corresponding tokenized product. When that step failed, the venue might return funds or challenge compensation, but it surely couldn’t flip the unique subscription into an allocation.

That is Half III of the RWA audit collection. Half I examined the asset layer. Half II traced trades and exits throughout swimming pools, quote routes, platform ledgers, and issuer workflows. This publish focuses on the alternate layer, the place the venue can flip the identical underlying publicity right into a by-product place, subscription stability, collateral entry, routed token switch, or redemption declare.

SpaceX entry cut up into a number of information

Pre-IPO perp (SPCXUSDT, Binance / Bybit) → artificial value exposureSPCXx marketing campaign (Binance Pockets, Bybit IPO Categorical) → subscription / allocation claimSPCXB (Binance bStocks) → substitute platform tokenNasdaq SPCX → brokerage shareBackpack SPCX (Solana) → pockets token + dealer redemption stackxStocks SPCXx (if delivered) → tracker certificates

Don’t collapse tickers. Nasdaq SPCX≠ xStocks SPCXx≠ Binance SPCXB ≠ Backpack Solana SPCX (SPCXxcqXj6e5dJDVNovHN8744zkbhM2bYudU45BimGb) ≠ SPCXUSDT perp.

Pre-IPO derivatives

Binance supplied SPCXUSDT pre-IPO perps earlier than itemizing day. Binance’s announcement states they don’t signify possession of the underlying share. Bybit listed SpaceX-linked SPCXUSDT pre-IPO perps per its announcement in the identical product class: margin and index publicity, not allocation or redemption.

I appeared on the pre-IPO perp tape individually in an earlier be aware. Right here, the perp is just one department of the broader exchange-layer object cut up.

CEX subscription and allocation claims

Bybit IPO Categorical opened June 7 to 11, 2026 with xStocks as tokenization companion per Bybit’s launch announcement. Funds locked till allocation; unused stability refunded. Marketing campaign supplies described professional rata allocation, not a assured fill. Binance’s Pockets SPCXx web page used the identical form: locked USDC, distribution not assured.

On IPO day each campaigns broke at allocation / supply, not subscription consumption. Bybit’s replace reported zero allocations and full refunds when xStocks couldn’t ship. Binance canceled SPCXx, refunded USDC, and airdropped SPCXB. The airdrop was $1M cut up by June 18 on a special ticker.

The supposed chain was:

CEX subscription stability → supplier allocation request → dealer stock or share allocation → authorized issuance → token supply → redemption availability

The general public proof locations the break after subscription consumption and earlier than token supply. It doesn’t find the precise failed hyperlink inside that interval.

The general public bulletins establish the failed step, however not the total upstream trigger. They don’t present whether or not the constraint was share allocation, dealer stock, custody readiness, authorized issuance, or one other supply dependency. The refund information affirm that the venues might reverse buyer balances. They don’t present that the venues or their supplier had secured the asset wanted to finish the unique product.

The subscription interface labored. The file chain did not.

This additionally raises a query for the subsequent layer of the audit. Binance might refund USDC and distribute a substitute token as a result of it managed the client ledger and knew the affected participant set. What if the identical failure occurred after subscriptions had moved via contracts, swimming pools, or a number of wallets?

My conjecture will not be {that a} decentralized system can’t restore the failure. It’s that restore would rely upon mechanisms outlined earlier than the failure: a refund path, participant snapshot, pause authority, improve key, governance course of, or funded compensation contract. With out a kind of paths, public settlement could make the failed state simpler to examine whereas making coordinated remediation slower and extra contested. The subsequent publish will look at that DEX-side drawback straight.

Backpack / Dawn Solana path

CoinDesk reported a same-day Solana launch with dealer redemption via Backpack’s stack. The mint and Jupiter token web page present that the token existed and may very well be surfaced for swaps. These information don’t set up who held the corresponding shares, when redemption was out there, or which dealer file managed the conversion. The on-chain leg makes switch and routing simpler to examine. The share entitlement nonetheless is dependent upon the brokerage stack described off-chain.

Issuer authorized wrapper (xStocks household)

xStocks official docs: every xStock is a tracker certificates with financial publicity; no voting rights; not direct fairness possession. IPO-access merchandise on xStocks inherit that object until a separate prospectus says in any other case.

Common framework: what RWAs turn out to be inside venues

Inside a venue, an RWA can turn out to be a platform stability, collateral enter, routed switch, or redemption declare. Every kind fails otherwise as a result of a special system decides whether or not the person can commerce, withdraw, pledge, or redeem.

The interface can subsequently succeed whereas a later step fails. A returned quote could disappear at a bigger dimension, and a platform stability can replace with out public settlement. Even a accomplished token switch leaves the separate redemption course of unresolved.

Three recurring venue capabilities

The circumstances beneath usually are not direct analogues. They present how the controlling file adjustments with the venue operate.

A. Kraken / xStocks: platform-record buying and selling path

xStocks-family tracker certificates on Kraken appear like a standard alternate product: ticker, stability, fill. The fill first adjustments Kraken’s buyer ledger. It doesn’t create a public token switch for every commerce.

This creates a three-record reconciliation drawback. Kraken information the client legal responsibility in its platform ledger; its basic Proof of Reserves program is a separate proof floor. The xStocks issuer reserve proof addresses the property backing the certificates construction, whereas the product phrases govern withdrawal and redemption. None of these information alone maps one buyer’s platform stability via the total custody and issuer chain. A failure can sit in platform accounting, withdrawal processing, issuer reserves, or redemption phrases even when the buying and selling display continues to indicate a stability.

B. OKX / BUIDL: collateral / risk-engine enter

BUIDL is a tokenized money-market fund curiosity for certified buyers. Below the April 2026 framework introduced by OKX, BlackRock, and Commonplace Chartered, eligible shoppers can pledge BUIDL as yield-bearing collateral whereas Commonplace Chartered gives off-exchange custody.

Right here, token possession is simply an enter. OKX’s threat engine should determine whether or not the place counts as collateral, what worth to acknowledge, and when liquidation can happen. A public switch can present that BUIDL moved to a custodian or accepted handle. It can’t present the collateral worth acknowledged by OKX or the circumstances underneath which the place will probably be launched or liquidated. The related audit threat is a mismatch between custody state and risk-engine state, not inadequate AMM liquidity.

C. Jupiter / xStocks: aggregator-mediated public settlement path

A Jupiter quote exposes extra of the execution path than a CEX fill as a result of the response can establish route legs and anticipated output. It’s nonetheless solely a quote. The route could change earlier than execution, value influence can develop with dimension, and a profitable swap says nothing about issuer redemption.

The June samples reviewed right here had been quote-level and mint-metadata-level proof, not executed transaction proof. They’re helpful for checking route composition, token controls, and value influence on the sampled dimension. They can not set up sturdy exit capability or make one pool the default xStocks market. That is the DEX-side failure mode: public execution proof is accessible, however liquidity can fragment throughout routes whereas the authorized exit stays exterior the swap.

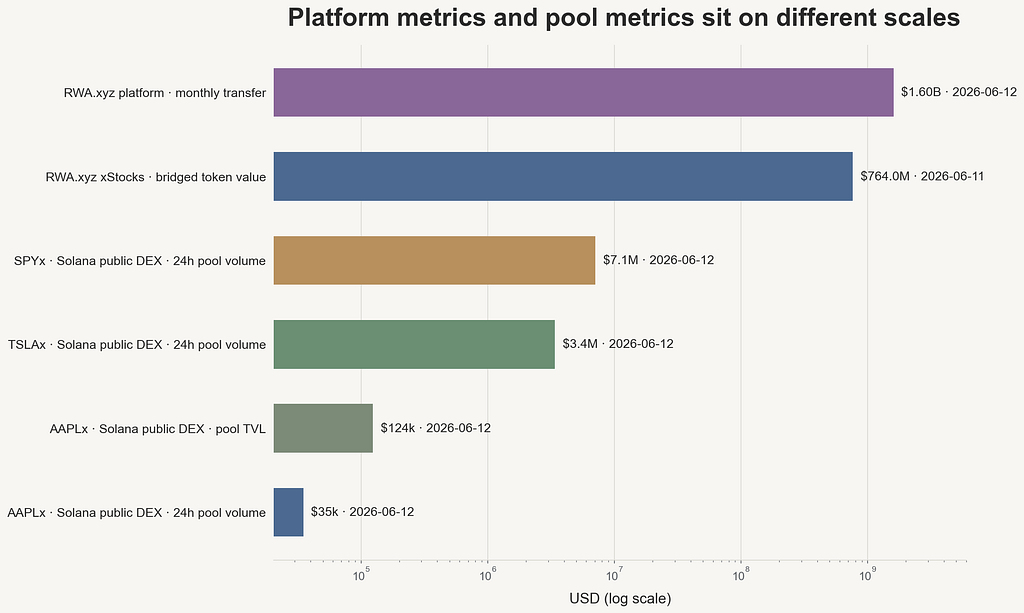

Metrics usually are not interchangeable

Fig. 3 places a number of xStocks measurements beside one another as a result of they’re simple to confuse:

RWA.xyz platform switch (~$1.03B April / $1.60B June 2026 on the xStocks platform web page; writer captures): wallet-to-wallet transfers on-chain in USD, not CEX buying and selling quantity.Bridged / distributed worth (~$764M in Fig. 3, June 11, 2026; author-captured): platform-scale inventory metric, not switch movement.Solana DEX pool TVL / quantity (AAPLx ~$124k / ~$35k 24h, author-captured GeckoTerminal snapshot June 12, 2026): public pool snapshot, not an IPO e book.Jupiter quote (author-captured AAPLx at $100k USDC, June 2026, ~68% value influence): one dimension, not exit capability.Platform refund information returned funds after a failed supply path.

Closing

RWA alternate is structurally multi-record. The buying and selling display, buyer ledger, token contract, custodian account, issuer register, dealer stock, and redemption workflow don’t turn out to be one authoritative file just because they share a ticker.

This isn’t opacity accidentally. Every file belongs to a special operate and sometimes a special establishment. The sensible query is which file controls the subsequent state transition. For an IPO marketing campaign, allocation and supply information determine whether or not a subscription turns into an asset. For collateral, the danger engine decides what worth can help a place. For an aggregator route, execution information proves the swap, whereas issuer phrases nonetheless management redemption.

Extra tokenization won’t essentially cut back this fragmentation. Including chains, bridges, aggregators, collateral programs, and automatic redemption paths creates extra state transitions that should agree. Composability expands entry, but it surely additionally expands the reconciliation floor.

The subsequent stage of RWA infrastructure subsequently wants greater than public tokens and visual transfers. It wants specific hyperlinks between information, outlined authority once they disagree, and remediation paths for the purpose the place the chain stops.

Appendix: proof and replica

Proof: egpivo/rwa-audit

rwa_xyz_platform_transfer_snapshots.jsonrwa-token-timeseries-export CSVgecko_aaplx_pools.jsongecko_tslax_pools.jsongecko_spyx_pools.jsonjupiter_quote_aaplx_100k.json

Reproduce the information with the command

cargo run – bin rwa-exchange-freeze

This publish was initially revealed on my private weblog: https://egpivo.github.io/2026/06/21/where-rwa-exchange-risk-actually-sits.html

The place RWA Alternate Danger Truly Sits was initially revealed in The Capital on Medium, the place individuals are persevering with the dialog by highlighting and responding to this story.

{kind=link}