Europe’s MiCA deadline has now entered the part by which licenses start to form distribution.

The primary wave of concern centered on which platforms European customers may nonetheless attain after July 1. The following part is extra structural. MiCA is deciding which issuers, banks, asset servicers, and app suppliers can proceed providing stablecoins and crypto merchandise to prospects throughout the regulated market.

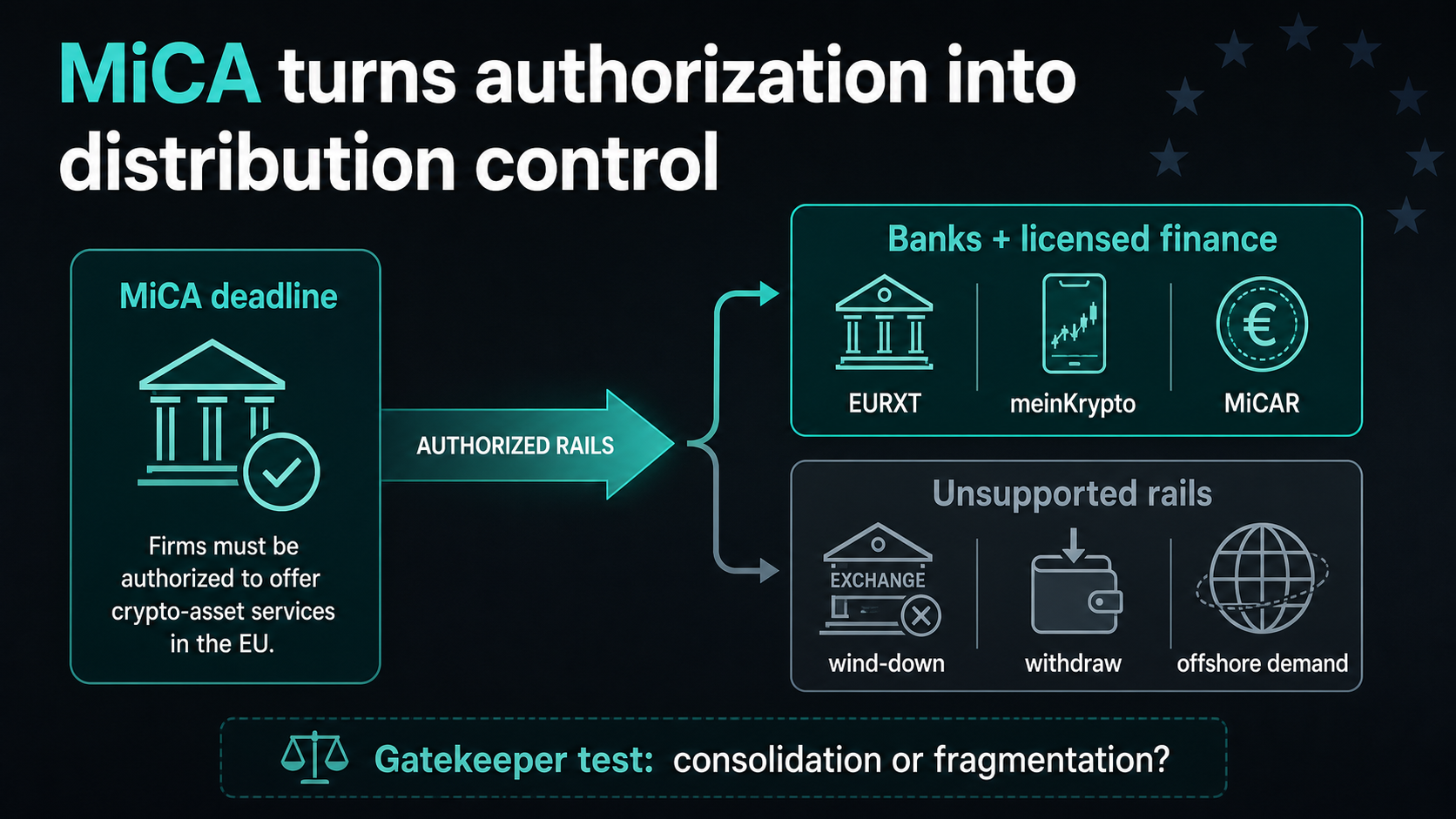

ESMA says MiCA creates uniform EU guidelines for crypto-asset issuers and repair suppliers, overlaying transparency, disclosure, authorization and supervision. Its interim MiCA register was final up to date on July 3, two days after the transitional interval for a lot of current crypto-asset service suppliers expired.

That timing issues as a result of the tip of the grandfathering interval adjustments MiCA from a licensing deadline right into a distribution filter. Approved corporations can hold serving the market. Unauthorized corporations should transfer towards exit, switch, or closure.

ESMA’s June 23 assertion informed unauthorized crypto-asset service suppliers to cease onboarding new EU shoppers, cease opening new shopper relationships or accounts, stop advertising and solicitation, and restrict exercise to steps wanted to promote, switch, reallocate or shut positions. Custody can proceed just for the strictly crucial interval for an orderly exit.

That’s the regulatory body. The market impact is sharper: MiCA is popping authorization right into a supply of distribution energy.

Banks are transferring into the hole

The clearest instance comes from inside conventional finance.

CACEIS mentioned Crédit Agricole launched EURXT on July 1 as a euro-denominated digital cash token issued on Ethereum by CACEIS. The group described it as MiCA-compliant, pegged to the euro, backed one-to-one by fiat euros and initially obtainable to institutional traders and company shoppers of CACEIS.

The primary use case was settlement for a subscription right into a tokenized Amundi cash market fund somewhat than a client pockets marketing campaign. That element exhibits the place compliant stablecoins could first acquire traction in Europe: inside asset servicing, fund settlement and bank-controlled institutional workflows.

CACEIS additionally mentioned EURXT’s reserves are made completely of money held on the steadiness sheet of CACEIS Financial institution. The token’s compliance pitch is subsequently greater than Ethereum issuance. The reserve, issuer, and shopper channels all sit inside a regulated monetary group.

That construction issues as a result of stablecoin competitors in Europe could more and more rely upon who can mix on-chain settlement with a regulated steadiness sheet, a trusted shopper base and a distribution channel that supervisors already perceive. A euro token issued by an asset servicer enters the market with a distinct path from an offshore greenback stablecoin in search of placement on crypto-native venues.

Germany’s cooperative banking sector is constructing the opposite aspect of the identical map.

DZ Financial institution mentioned it obtained BaFin MiCAR authorization on the finish of December 2025 for meinKrypto, a pockets and buying and selling service that can be built-in into the VR Banking App. Taking part Volksbanken and Raiffeisenbanken nonetheless have to receive their very own BaFin notification and implement it earlier than providing it, however as soon as they full these steps, prospects can put money into crypto absolutely digitally by the banking app.

The launch set consists of Bitcoin, Ethereum, Litecoin and Cardano. DZ Financial institution additionally cited a September 2025 Genoverband research, which mentioned greater than one-third of cooperative banks deliberate to introduce the crypto resolution within the following months.

CryptoSlate’s Ethereum web page listed ETH at about $1,763.10 on July 5, whereas CACEIS’ use of Ethereum exhibits how public-chain settlement can nonetheless be routed by bank-issued devices.

That may be a distribution story. A self-directed buyer can entry crypto by the banking app they already use, somewhat than trying to find a separate platform. If sufficient cooperative banks implement the service, MiCA-compliant entry turns into a part of peculiar account infrastructure.

USDT exhibits the opposite aspect of the filter

The financial institution rollout is going on as dollar-stablecoin entry faces extra platform-by-platform danger in Europe.

WuBlockchain reported on X on July 4 that Revolut is phasing out USDT help for European customers. The reported timetable says customers can purchase USDT till July 6; new deposits cease on July 30; promoting or withdrawing to exterior wallets stays obtainable till August 31; and remaining balances are transformed to fiat after that date.

The delisting suits the broader MiCA sample: platforms should determine whether or not supporting a token, an issuer, or a service creates extreme regulatory publicity after the deadline.

MiCA addresses authorization and compliance dangers somewhat than instantly prohibiting USDT. If a big retail app decides {that a} token not suits its European compliance path, the sensible outcome for customers can resemble a lack of entry, even when the authorized mechanism is licensing and platform danger administration.

The stakes are giant as a result of USDT is market infrastructure. CryptoSlate’s Tether web page listed USDT at about $184.11 billion in market worth and $45.56 billion in 24-hour quantity on July 5. It’s one in every of crypto’s essential greenback settlement and buying and selling rails.

The broader CryptoSlate coin rankings confirmed a $2.17 trillion crypto market and $52.38 billion in 24-hour quantity yesterday, July 5, with USDT rating third by market capitalization behind Bitcoin and Ethereum.

That scale is why the post-deadline query reaches past one fintech and one token. Europe is testing whether or not regulated venues could make compliant euro-denominated devices helpful sufficient to compete with the liquidity habits constructed round USDT. If they’ll, MiCA redirects stablecoin entry towards issuers and distributors contained in the bloc. If they can’t, customers could hold trying to find greenback liquidity exterior the supervised perimeter.

The distinction between these outcomes will present up in venue help, app availability, pockets flows and settlement use instances somewhat than in a single authorized announcement. Each platform choice turns into one other sign about the place stablecoin demand is being routed.

The moat is compliance plus distribution

MiCA was written as a harmonized rulebook for investor safety, market integrity and monetary stability. These goals matter, particularly for customers who had been uncovered to platforms working beneath uneven nationwide regimes.

However regulation additionally adjustments market construction. After July 1, a compliant issuer or financial institution holds greater than a license. It has a channel that rivals can’t match throughout the EU with out authorization.

Crédit Agricole and CACEIS can place a euro stablecoin in tokenized fund settlement. DZ Financial institution can embed crypto buying and selling contained in the cooperative banking community’s app infrastructure. Licensed exchanges and brokers can take up customers leaving non-compliant platforms. In the meantime, merchandise exterior the MiCA perimeter rely upon offshore entry, self-custody, or platforms keen to soak up the compliance danger.

That’s the gatekeeper impact. It’s much less dramatic than a sudden prohibition, however it could be extra sturdy. Distribution in finance usually belongs to whoever owns the trusted account, the settlement workflow, and the shopper relationship. MiCA is making these benefits extra precious in crypto.

The outcome might be cleaner, safer entry for customers who transfer to approved rails. It may additionally give giant banks, asset servicers and licensed finance teams a structural benefit over crypto-native corporations that battle to safe approval, keep native compliance groups or protect token protection beneath the brand new guidelines.

CryptoSlate has already coated the first-order MiCA questions: Binance and USDT liquidity, and the user-migration take a look at created by the July 1 deadline. The following take a look at is who advantages after these migrations occur.

One path is clear consolidation. Compliant banks, asset servicers, and licensed exchanges take up extra exercise, euro-denominated EMTs acquire wider use in actual settlement, and customers get clearer protections.

The opposite path is fragmentation. Customers hold chasing USDT liquidity exterior licensed European rails, offshore platforms hold serving demand from past the perimeter, and the EU positive aspects a cleaner rulebook with out capturing the flows it most desires to oversee.

The reply as to whether MiCA makes banks the subsequent stablecoin gatekeepers is subsequently conditional however sturdy. The legislation doesn’t hand banks management by itself. It makes authorization, custody, reserve construction and app distribution the gates by which compliant crypto entry now has to cross.

Within the first week after the deadline, these gates are already trying extra like financial institution doorways.

{kind=link}