Intuitive Surgical has a powerful long-term observe report, however has not had a terrific YTD or one-year efficiency. The Day by day Breakdown digs in. Focused on extra Deep Dive content material? Try our newest analysis.

Deep Dive

Regardless of a $160 billion market cap and a 556% return over the past decade, Intuitive Surgical should fly below the radar for a lot of buyers. That stated, shares are down about 25% from their highs and have fallen nearly 15% over the previous yr.

The corporate develops applied sciences that assist physicians carry out minimally invasive procedures worldwide. Its key merchandise embrace the da Vinci Surgical System for complicated surgical procedures and the Ion endoluminal system for lung biopsies. The corporate additionally offers devices, coaching, companies, and digital instruments to assist robotic surgical procedure packages.

For years, Intuitive Surgical has been a gentle operator throughout the healthcare area. Like many others although, it noticed some lumpiness in its enterprise from 2020 to 2022. Since then, it’s been comparatively clean crusing for earnings, income, and recurring income:

Future Progress Projections

Wanting forward, analysts count on fairly constant outcomes of Intuitive Surgical, with anticipated annual earnings and income development within the 13% and 16% vary. In accordance with Bloomberg, analysts challenge the next:

Earnings Progress: 15.8% in 2026, 13.6% in 2027, and 13.8% in 2028

Income Progress: 16.4% in 2026, 13.2% in 2027, and 13.1% in 2028

Analysts at present have a consensus worth goal of ~$576 on ISRG inventory, implying about 27% upside to right this moment’s inventory worth.

Wish to obtain these insights straight to your inbox?

Join right here

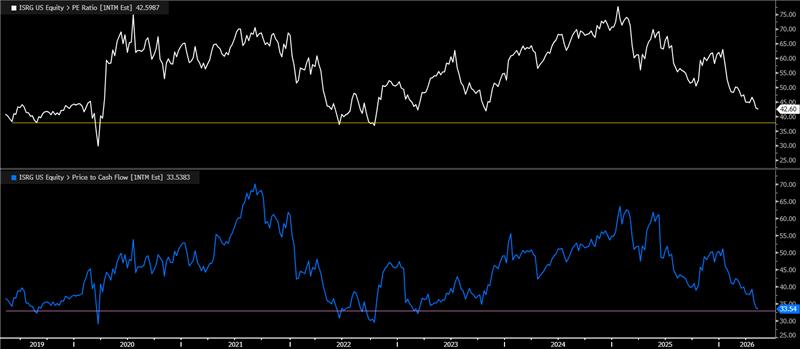

Diving Deeper — Valuation

Mid-teen development charges are very strong and characterize regular growth. Nevertheless, there could also be some hesitancy from buyers to pay up for ISRG inventory for development that’s sturdy, however not essentially out of this world. That’s the place valuation-focused buyers could get hung up on Intuitive Surgical.

On the one hand, ISRG is buying and selling at its lowest ahead price-to-earnings ratio in nearly three years (white line). Nevertheless, it’s nonetheless above the valuation zone of 38x or decrease, which has marked a trough since 2019. On a ahead price-to-FCF foundation (blue line), the inventory is close to a trough zone of roughly 33x. On the finish of the day although, some may nonetheless argue that this valuation is an excessive amount of for mid-teen development.

Dangers

Key dangers for Intuitive Surgical embrace its heavy reliance on da Vinci process development, which could be pressured by hospital staffing points, elective-surgery traits, and tighter hospital budgets. The corporate additionally faces execution danger across the da Vinci 5 improve cycle, rising competitors in surgical robotics, tariff and margin pressures, and China-specific dangers tied to pricing, reimbursement, quotas, and native opponents. In the meantime, slower adoption of newer platforms like Ion, potential regulatory or issues of safety, and ISRG’s premium valuation depart little room for disappointment.

The Backside Line

Intuitive Surgical has change into a blue-chip inventory throughout the medical system business. Nevertheless, shares have struggled much less as a result of the enterprise is damaged and extra as a result of the inventory was priced for perfection. Expectations have been sky-high, margins have been below scrutiny, and buyers are questioning whether or not development can maintain justifying the premium a number of.

Because the inventory worth has come down, buyers at the moment are questioning whether or not a long-term alternative is in entrance of them or if it’s a crimson warning flag to remain away.

Disclaimer:

Please word that as a result of market volatility, among the costs could have already been reached and situations performed out.

{kind=link}