Charles Schwab, Constancy, and JPMorgan Are All In on Crypto Now. Right here Is Precisely What They’re Shopping for

When the three greatest names in American finance all make the identical guess in the identical 12-month window, it stops being a coincidence and begins being a sign.

For years, the official Wall Avenue line on cryptocurrency went one thing like this: unstable, unregulated, speculative — possibly a curiosity for retail merchants, however actually not a spot for severe institutional cash. Jamie Dimon famously referred to as Bitcoin a “fraud” in 2017. Constancy was the quiet outlier, constructing infrastructure within the background whereas its friends scoffed. Charles Schwab stored crypto at arm’s size, providing futures publicity whereas staying fastidiously away from precise digital belongings.

That period is over.

In a compressed and dramatic stretch spanning late 2025 into mid-2026, Charles Schwab, Constancy, and JPMorgan Chase have every made strikes that may have appeared unthinkable simply three years in the past. This isn’t about dabbling. That is about three establishments that collectively handle trillions of {dollars} in shopper belongings deciding that crypto is now not a class they’ll afford to sit down out. The query value asking — the one most retail traders aren’t asking loudly sufficient — is: what, particularly, are they shopping for? And what does it imply that they’re all shifting at as soon as?

The Regulatory Unlock That Made All of This Attainable

Earlier than entering into what every establishment is doing, it’s essential to perceive why they’re doing it now. As a result of the timing isn’t unintentional.

A sequence of regulatory shifts quietly dismantled the authorized boundaries that had stored main banks and brokerages on the sidelines. In March 2025, the FDIC rescinded its prior-approval requirement for banks participating in permissible crypto actions — a coverage that had functioned as an efficient veto on bank-level crypto participation. Two months later, in Might 2025, the OCC issued steerage clarifying that nationwide banks may purchase and promote customer-custodied crypto belongings and outsource execution with correct danger administration. By February 2026, Constancy had obtained OCC approval for bank-based crypto custody and execution outright.

The SEC adopted in April 2026 with an interim assertion clarifying broker-dealer registration for sure crypto interfaces. And underpinning all of it was the passage of the GENIUS Act, which created a federal framework for stablecoin laws for the primary time. Mixed, these adjustments didn’t simply cut back uncertainty — they handed the largest establishments in finance a authorized roadmap to construct on.

Wall Avenue had been watching and ready. As soon as the runway was cleared, they didn’t stroll. They sprinted.

Charles Schwab: Spot Bitcoin and Ethereum, Beginning Now

Schwab’s transfer is the one most retail traders ought to take note of, as a result of it straight adjustments what 35 million brokerage purchasers can do inside an account they already have.

In Might 2026, Charles Schwab started rolling out spot cryptocurrency buying and selling, beginning with Bitcoin and Ethereum. This isn’t crypto futures, not an ETF, not an oblique publicity automobile — that is direct possession of the underlying digital belongings, accessible by means of the identical interface Schwab purchasers already use to purchase Apple inventory or Treasury bonds.

The strategic logic behind the launch is just not difficult, however it’s vital. Schwab already estimates that its purchasers maintain roughly 20% of the US spot crypto exchange-traded product market — that means roughly one in 5 {dollars} invested in Bitcoin and Ethereum ETFs already sits inside a Schwab account. These purchasers have been going elsewhere to carry the precise cash. Schwab, in impact, has been watching a income stream stroll out the door, and it has now determined to cease letting that occur.

Schwab has been specific that Bitcoin and Ethereum are just the start. The agency has indicated plans to broaden past these two belongings and add switch functionality over time, that means purchasers will finally have the ability to transfer crypto between Schwab and exterior wallets. Internally, Schwab has additionally been exploring the event of a stablecoin — a transfer that may place it to play in blockchain-based settlement and liquidity, not simply as a buying and selling venue however as a monetary infrastructure supplier.

For context on the demand it’s strolling into: visits to Schwab’s crypto platform surged 90% year-over-year heading into the launch. The pent-up curiosity was by no means the query. The regulatory and operational infrastructure simply wanted to catch up.

Constancy: The Veteran Enjoying Its Deepest Playing cards

Constancy has been essentially the most crypto-forward of the foremost conventional brokerages for years. It launched the Constancy Smart Origin Bitcoin Fund (FBTC) in 2024, which now holds $13.4 billion in belongings beneath administration. It has run Constancy Digital Belongings, a devoted institutional crypto custody and buying and selling operation, since 2018. It sponsored an Ethereum ETF alongside its Bitcoin fund. It’s not a newcomer to this area.

What modified in 2026 is the regulatory standing of these operations. With OCC approval secured in February 2026 for bank-based crypto custody and execution, Constancy can now function its digital asset infrastructure beneath the identical regulatory umbrella as its standard banking actions. That issues as a result of it adjustments who can entry these providers — particularly, it opens doorways with institutional purchasers like pension funds and endowments which have strict counterparty and regulatory necessities.

Constancy’s positioning within the institutional market is especially aggressive. Its Digital Belongings analysis workforce has revealed steerage recommending that long-term traders goal 0–5% crypto publicity in a portfolio, with the specific argument that even a 2% allocation to Bitcoin improves annual retirement spending capability by 1–4% whereas growing loss danger by lower than a proportion level. For an asset administration agency of Constancy’s scale, that form of analysis publication is just not impartial commentary — it’s a shopper schooling technique designed to maneuver allocation habits.

Constancy presently holds extra Bitcoin beneath administration by means of its ETF merchandise than almost every other agency besides BlackRock. As of late 2025, Constancy’s FBTC was the constant second-place issuer within the US spot Bitcoin ETF market by influx quantity, usually pulling in tons of of tens of millions of {dollars} in single-day inflows. The aggressive moat it has in-built digital asset custody and ETF infrastructure over eight years of early funding is now paying off in a market that has decisively gone institutional.

JPMorgan: The Blockchain Play No One Is Speaking About Loudly Sufficient

JPMorgan’s crypto technique is extra advanced than Schwab’s or Constancy’s — and arguably extra consequential. Whereas the financial institution’s CEO has remained publicly skeptical of decentralized cryptocurrency as an asset class, JPMorgan’s operational strikes inform a really completely different story.

The financial institution’s Kinexys platform (previously identified for JPM Coin) has been processing institutional funds on a non-public blockchain since 2020. As of 2026, that platform processes over $1 billion in each day transactions, primarily in company treasury operations and cross-border fee settlements. Its Onyx division has expanded into tokenized collateral networks, programmable funds for company purchasers, and repo transaction platforms.

However essentially the most vital improvement got here in 2026, when JPMorgan launched a tokenized deposit token on Base — Coinbase’s public Layer 2 community constructed on Ethereum. It is a vital public sign from a financial institution that had beforehand confined its blockchain operations to non-public, permissioned networks. Transferring onto a public blockchain signifies that JPMorgan now views interoperability with the broader crypto ecosystem as an asset slightly than a danger.

In December 2025, JPMorgan additionally started exploring institutional spot crypto buying and selling — a riskless principal mannequin that permits the financial institution to facilitate trades with out holding crypto stock by itself stability sheet, lowering counterparty danger whereas capturing buying and selling payment income. This mirrors the identical path Schwab has taken with its personal custody and execution mannequin.

After which there may be the tokenized deposit community. In June 2026, JPMorgan, Citi, Financial institution of America, and different main US banks introduced plans to construct a shared tokenized deposit community, operated by The Clearing Home, focusing on a launch by mid-2027. The specific strategic objective: to compete with stablecoins. If prospects start holding {dollars} in stablecoin type at scale, banks face deposit flight. The tokenized deposit community is designed to offer blockchain-native fee capabilities — 24/7 settlement, prompt switch, programmable cash — whereas retaining deposits inside the regulated banking system.

For JPMorgan, crypto is just not a product class. It’s an infrastructure struggle.

What $59 Billion in ETF Inflows Truly Tells You

Zoom out from the person agency methods and a broader sample comes into focus. US spot Bitcoin ETFs have now collected over $59 billion in cumulative web inflows since their January 2024 approval. In Might 2026 alone, Bitcoin ETFs registered over $1.6 billion in month-to-month inflows, even amid market volatility. BlackRock’s IBIT holds over $66 billion in belongings. Constancy’s FBTC holds over $13 billion. Ethereum ETFs have attracted tons of of tens of millions in institutional inflows alongside them.

The composition of that capital is just not retail cash chasing headlines. It’s pension plans, household places of work, endowments, and institutional allocators making structured, long-term portfolio choices by means of regulated automobiles. Based on analysis from the institutional sector, 68% of institutional traders now both maintain or plan to put money into Bitcoin ETFs. That quantity would have been unrecognizable 4 years in the past.

The institutional thesis for Bitcoin and Ethereum is now standardized sufficient to be put in a prospectus. The belongings have liquidity. They’ve custody options from certified custodians. They’ve worth discovery by means of regulated markets. They’ve allocation frameworks revealed by Constancy, VanEck, and others. The remaining friction for many allocators is basically reputational and operational — and corporations like Schwab eradicating the operational friction is exactly what accelerates the reputational shift.

What This Means If You’re a Retail Investor

The entry of Schwab, Constancy, and JPMorgan into direct crypto providers adjustments the calculus for retail traders in a number of methods which are simple to underestimate.

First, it adjustments entry. Thousands and thousands of traders who held again from crypto as a result of they didn’t wish to open a Coinbase account, handle a software program pockets, or navigate an unfamiliar interface can now entry Bitcoin and Ethereum by means of the identical brokerage they’ve used for many years. Friction is a real barrier, and Schwab simply eliminated it for 35 million individuals.

Second, it adjustments notion. When establishments of this measurement and popularity make structured bets on digital belongings, it strikes the Overton window for what counts as a official funding. Crypto in your Constancy retirement account seems to be completely different from crypto on a speculative trade — not as a result of the asset modified, however as a result of the context did.

Third — and that is the purpose most commentators miss — it adjustments liquidity. Each main monetary establishment that provides crypto custody and buying and selling infrastructure will increase the depth and stability of these markets. It reduces the dominance of crypto-native exchanges in worth formation. It creates extra institutional counterparties and extra mechanisms for big capital to maneuver out and in effectively.

None of this eliminates Bitcoin’s volatility, Ethereum’s execution dangers, or the real uncertainty round the place crypto matches long-term in a diversified portfolio. These aren’t endorsements; they’re observations in regards to the structural path of the market.

The Backside Line

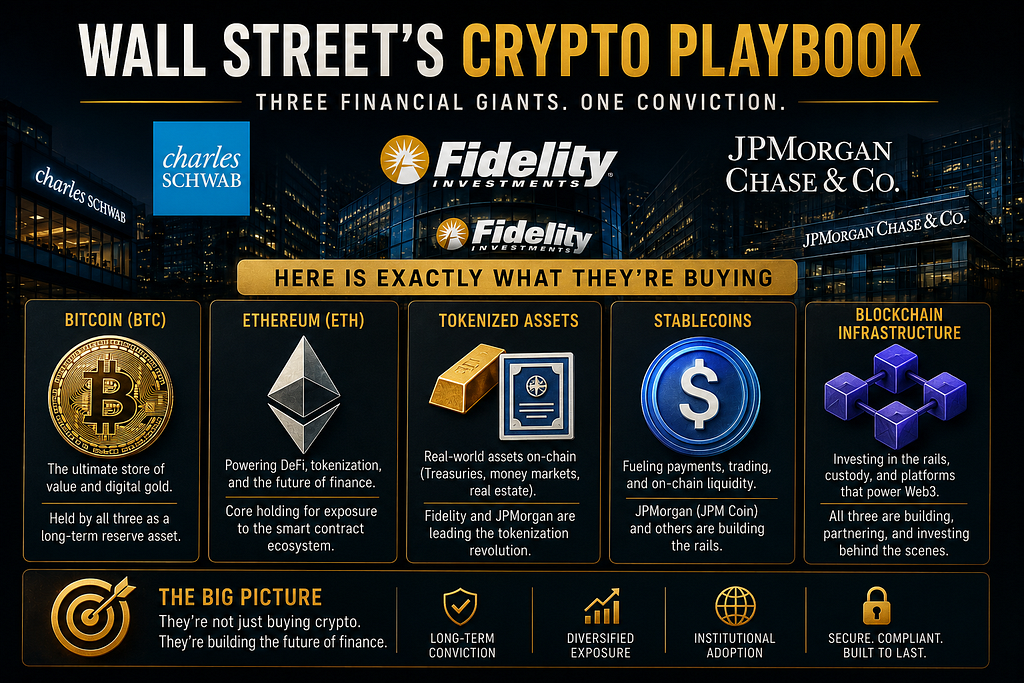

Schwab is shopping for Bitcoin and Ethereum — and bringing 35 million purchasers alongside for the journey. Constancy is shopping for Bitcoin, Ethereum, and regulatory infrastructure that lets it custody these belongings contained in the regulated banking system. JPMorgan is shopping for the rails: blockchain fee infrastructure, tokenized deposits, and a stake sooner or later structure of how cash strikes.

Three completely different methods. Three completely different positions on the risk-reward spectrum. One shared conclusion: the monetary system is integrating crypto, not as a fringe asset class, however as a everlasting part of recent market infrastructure.

The query is now not whether or not Wall Avenue is in on crypto. They’re, demonstrably, irrevocably, and with billions of {dollars} of dedicated capital and infrastructure funding behind them.

The query now’s whether or not the remainder of us had been paying consideration whereas it occurred.

This text is for informational functions solely and doesn’t represent monetary or funding recommendation. Cryptocurrency investments carry vital danger. At all times conduct your individual analysis earlier than making any funding choices.

Charles Schwab, Constancy, and JPMorgan Are All In on Crypto Now. was initially revealed in The Capital on Medium, the place persons are persevering with the dialog by highlighting and responding to this story.

{kind=link}