$WISE.L is a progress firm, with the profitability of a money cow, and the valuation of a gradual grower.

Key Highlights:

Smart provides worthwhile progress in a rising area of interest

The corporate is constructing a large moat and sharing the advantages with its purchasers

In a worst-case state of affairs, returns can be constructive

The enterprise:

WISE is an organization that facilitates worldwide cash transfers. They at the moment have a market share of lower than 5% of cash moved by individuals, and fewer than 1% of the market share of cash moved by small companies.

Supply: Firm’s FY 2025 earnings launch

For additional reference concerning the enterprise, you’ll be able to verify THIS earlier publish by @Rayeiris, shared beforehand, and that describes completely all the pieces about WISE.

How they’re constructing their moat:

Worldwide cash transfers have been traditionally very pricey for people. As an expat, I’ve skilled this earlier than. The charges that Smart’s opponents cost to prospects are unrealistically costly, however there was no different till Smart arrived. You would suppose that, to be a worthwhile firm, the take charges (what the corporate earns with every transaction) must be excessive. However as a matter of truth, Smart has been rising income and rising earnings whereas decreasing take charges.

Supply: Firm’s FY 2025 earnings launch

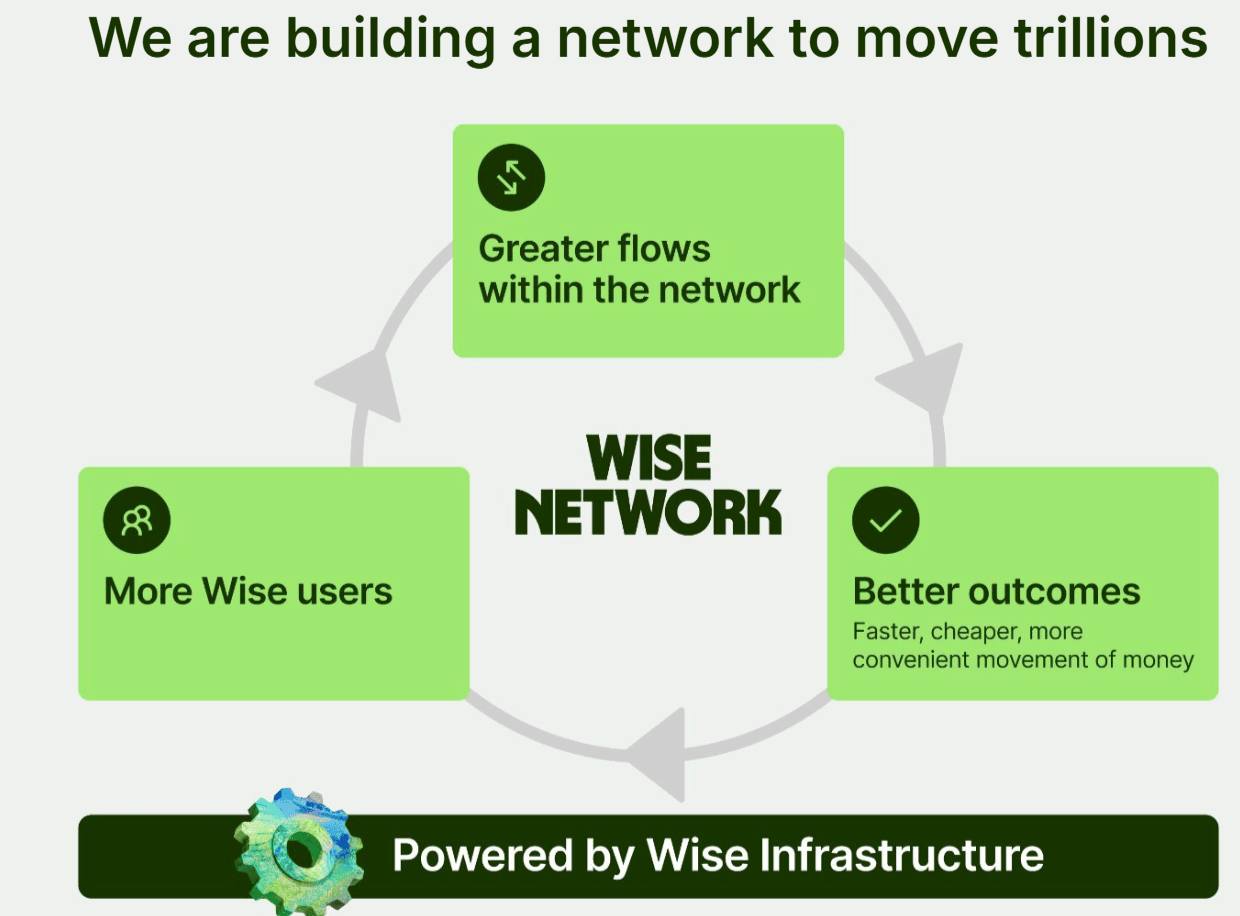

This can be a confirmed strategy to develop a MOAT: You get advantages from scale, and also you share it with prospects. Prospects see the advantages and use your product extra, bringing extra advantages for the corporate which might be shared with the client. It’s a virtuous circle that feeds itself.

Supply: Firm’s FY 2025 earnings launch

That is how Costco used to construct its MOAT. And it has labored splendidly for them through the years. However there’s a lot extra to it than solely cash transfers for people.

The corporate can also be increasing into new merchandise, like its Smart account for companies. They’re additionally together with new options like fast pay with a QR code. However extra importantly, with Smart Platform, companies, banks, and different organizations can profit from Smart’s infrastructure to switch cash overseas. Corporations like Morgan Stanley, NU, Normal Chartered, or Google Pay have already joined, displaying the potential of this product.

Valuation:

The corporate has established a long-term underlying revenue of 13%-16%, which is decrease than its present underlying revenue margin (24%). With a income progress of 15%-20%, and an curiosity revenue progress of 10%-20% (at the moment over 70% year-over-year), the risk-reward ratio appears to be like very compelling.

This mainly signifies that within the worst-case state of affairs, with a PE ratio of 20 instances earnings (which is a derating from its present a number of of over 28 instances), the corporate will ship an annual return of 1.77%. Then again, if the corporate retains delivering progress and profitability, with a PE ratio of 30 instances earnings, the corporate might ship a yearly return of over 20% per 12 months.

Dangers:

Income slowdown

Decrease rates of interest

All valuations think about income progress and progress within the curiosity revenue above 1%. If rates of interest go down considerably, this portion of the revenue might vanish. Additionally, if extra opponents, together with massive banks, enter the sphere with aggressive costs, income might be flat, and the revenue margin might be harmed.

Mitigating dangers:

Money and time-consuming course of for opponents to catch up

Development in balances held by prospects

Smart has constructed a robust moat for greater than 8 years now. If a competitor needed to duplicate this, it might be time-consuming and costly. Additionally, even when cash might speed up the method for a competitor to get the place Smart is, among the work isn’t about constructing the infrastructure itself, however about negotiating with third events and native regulatory our bodies, which is a gradual course of.

Concerning a decrease rate of interest state of affairs, it might be offset by larger balances held by prospects. Really, within the present atmosphere, though rates of interest are falling, the corporate is rising its curiosity revenue because of larger balances, which can probably be sustained sooner or later.

Conclusion:

Smart is doubtlessly a multibagger. A top quality enterprise creating a large moat whereas being very worthwhile. Given the area of interest the corporate is aiming at, competitors is scarce and provides worse circumstances than Smart. Any competitor eager to compete at the moment would want to sacrifice profitability for a very long time.

Catalysts:

Incorporation of extra firms into its Smart Platform, particularly banks

Sustained progress

Stabilization of its take fee

I personal a place in $WISE.L on the time of writing.

This communication is for info and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a proposal of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out considering any specific recipient’s funding aims or monetary state of affairs, and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index, or a packaged funding product are usually not, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}