1. Introduction

Greggs, the UK’s main bakery chain, has lengthy been a staple on British streets, famend for its inexpensive and handy meals on the go. Nevertheless, the financial panorama within the UK is shifting, presenting new challenges. Regardless of these pressures, Greggs continues to broaden, posting sturdy monetary efficiency and refining its strategic method to maintain progress.

For buyers, the query stays: Is Greggs well-positioned to face up to these challenges and ship long-term worth? This text delves into Greggs’ monetary efficiency, the broader financial context, and the strategic initiatives that might assist the corporate navigate unsure occasions.

2. Monetary Efficiency: A Balancing Act

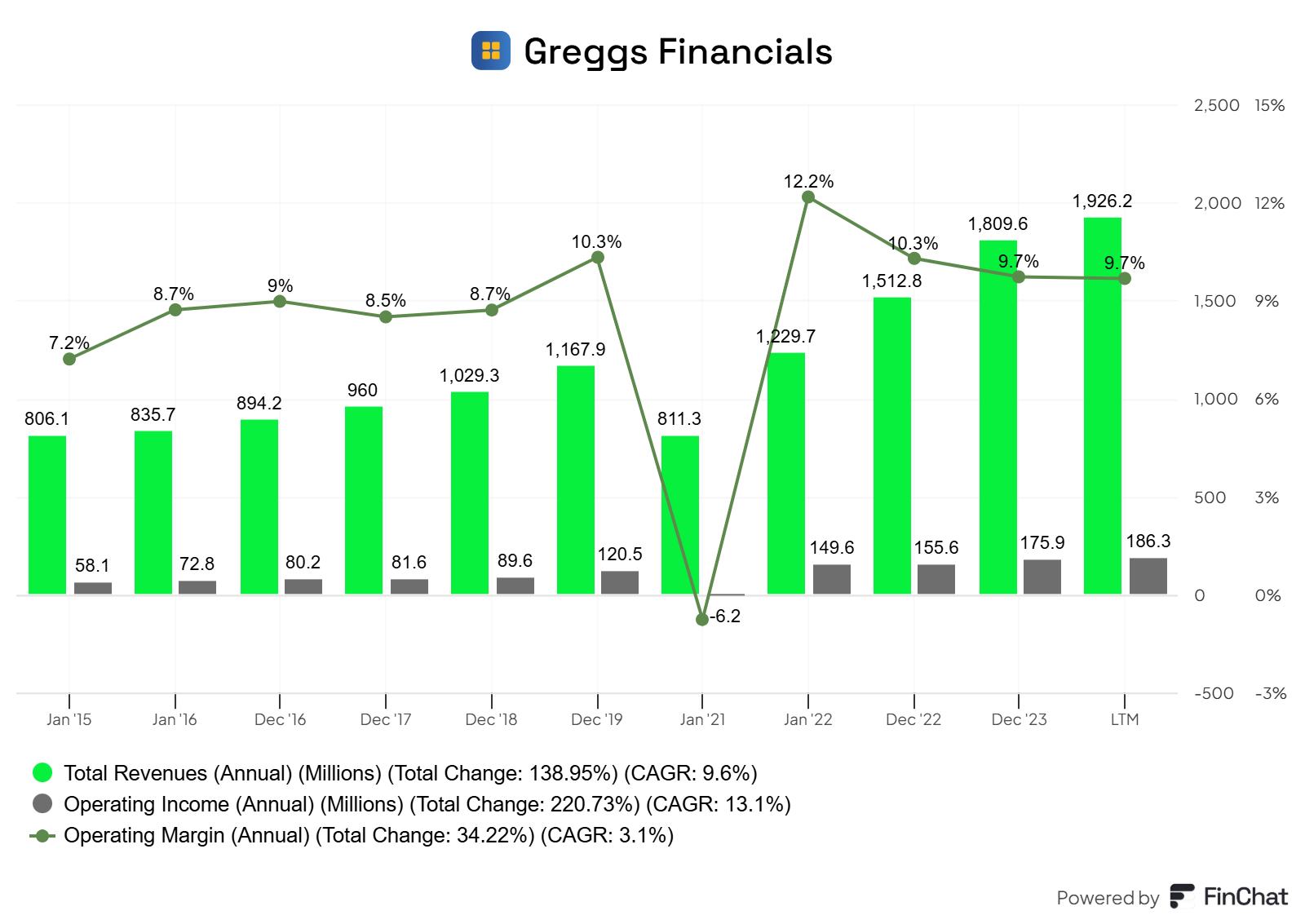

Greggs reported sturdy financials for 2024, with complete gross sales reaching £2.014 billion, reflecting an 11.3% year-over-year improve. Like-for-like (LFL) gross sales in company-managed shops rose by 5.5%, underscoring shopper resilience.

Nevertheless, a notable deceleration in gross sales progress was noticed all year long:

First half of 2024: 7.4% LFL gross sales progress

Third quarter: 5.0% progress

Fourth quarter: 2.5% progress

Greggs’ administration attributes this slowdown to lowered foot site visitors on excessive streets, signaling that even sturdy manufacturers aren’t proof against macroeconomic forces.

Supply: Greggs filings, Writer evaluation

From an operational perspective, Greggs’ value construction stays below strain. Inflationary pressures have elevated bills associated to uncooked supplies and wages affected by the will increase in Nationwide Minimal Wage and the extra nationwide insurance coverage contributions, impacting total profitability. In response, Greggs has applied selective value hikes, akin to growing the value of its iconic sausage roll from £1.20 final 12 months (was £1 in 2022) to £1.30, representing an 8% improve.

Supply: Finchat.io, Word: This chart doesn’t embrace the most recent 2 quarters as Greggs doesn’t report profitability metrics within the quarterly outcomes.

Regardless of these value pressures, the corporate’s operational efficiencies and economies of scale have helped mitigate margin erosion, demonstrating the resilience of its enterprise mannequin. In consequence, working margins at ranges near 10% stay above these seen within the pre-pandemic durations (besides 2019 that stood at 10.3%).

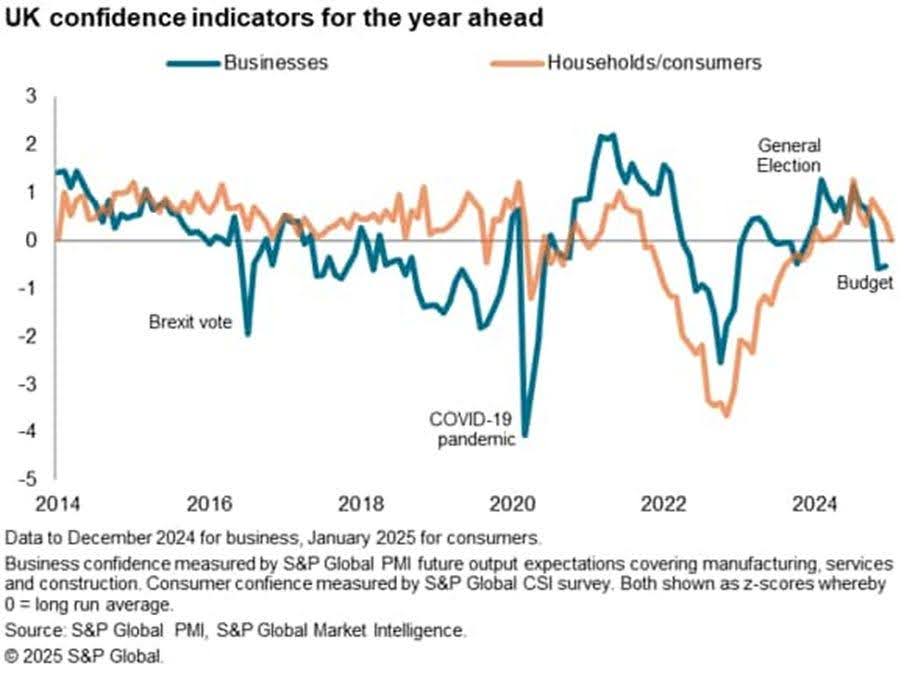

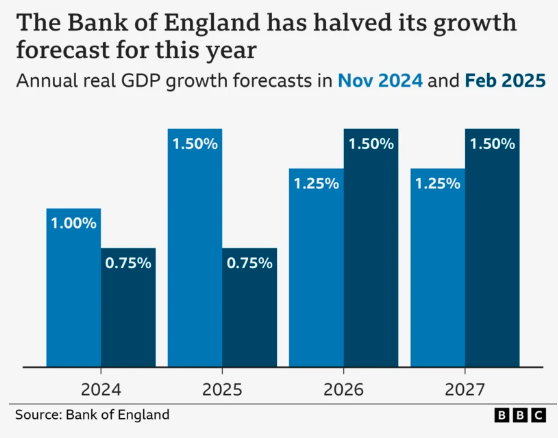

3. Financial Headwinds: GDP and Client Confidence

The UK financial system is presently going through a difficult interval, with weak shopper confidence and stagnant GDP progress reshaping spending habits. Though the Financial institution of England not too long ago lowered rates of interest from 4.75% to 4.5%, this transfer appears inadequate to drive progress.

This chart additionally highlights the insecurity amongst each customers and households, following the latest funds announcement.

Moreover, the Financial institution of England has revised its GDP progress forecast, slashing its 2025 progress projection to only 0.75%, whereas inflation is predicted to hit 3.7% by year-end. These components counsel that the UK is getting into a stagflationary atmosphere, elevating considerations in regards to the future progress prospects of food-on-the-go retailers akin to Greggs.

4. Strategic Initiatives: Progress Amid Uncertainty

Regardless of financial headwinds, Greggs stays dedicated to its long-term progress technique. A number of key initiatives underpin its resilience and potential for continued success.

Retailer Enlargement and Market Penetration

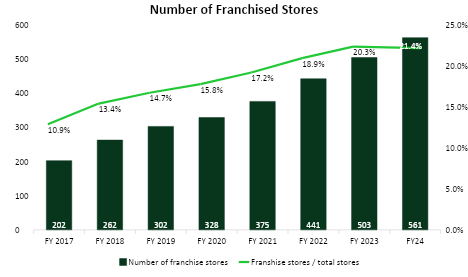

Greggs continues to broaden its bodily footprint, opening 145 new shops in 2024, bringing its complete areas to over 2,600 shops. The corporate goals to achieve 3,500 shops nationwide, capitalizing on sturdy model loyalty and geographic enlargement alternatives.

Supply: Greggs filings, Writer evaluation

Key parts of its enlargement technique embrace:

Extra Drive-Thrus: Catering to the rising demand for comfort, notably outdoors city facilities.

New Codecs: Smaller grab-and-go shops and retail park areas to diversify its attain.

Franchise Partnerships: Collaborating with third-party operators to speed up enlargement.

Supply: Greggs filings, Writer evaluation

This aggressive enlargement technique indicators confidence in future long run demand, however the sustainability of this progress hinges on financial stability.

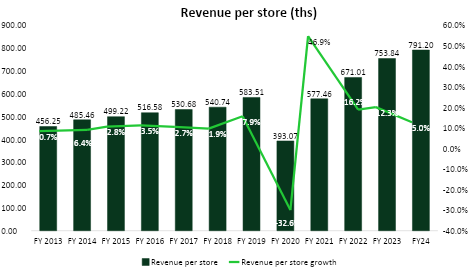

Digital Transformation, Supply Progress and Extra

Recognizing evolving shopper habits, Greggs has closely invested in digital transformation. The corporate has strengthened its supply partnerships with Uber Eats and Simply Eat, increasing its attain past conventional brick-and-mortar gross sales. Digital ordering and loyalty applications play a key position in its technique, driving buyer engagement and retention.

In H1 2024, 18.3% of transactions at company-owned shops had been scanned by way of the Greggs App, up from 10.6% final 12 months, signaling improved buyer loyalty. In the meantime, supply gross sales grew to six.7% of complete gross sales, in comparison with 5.3% in H1 2023.

One other key progress driver is night gross sales, that are outpacing the corporate’s total like-for-like progress. Night commerce caters to a wider vary of customers past breakfast hours.

These developments all level to 1 factor: increased income per retailer. With constant execution, Greggs is well-positioned for sustained enlargement.

Supply: Greggs filings, Writer evaluation

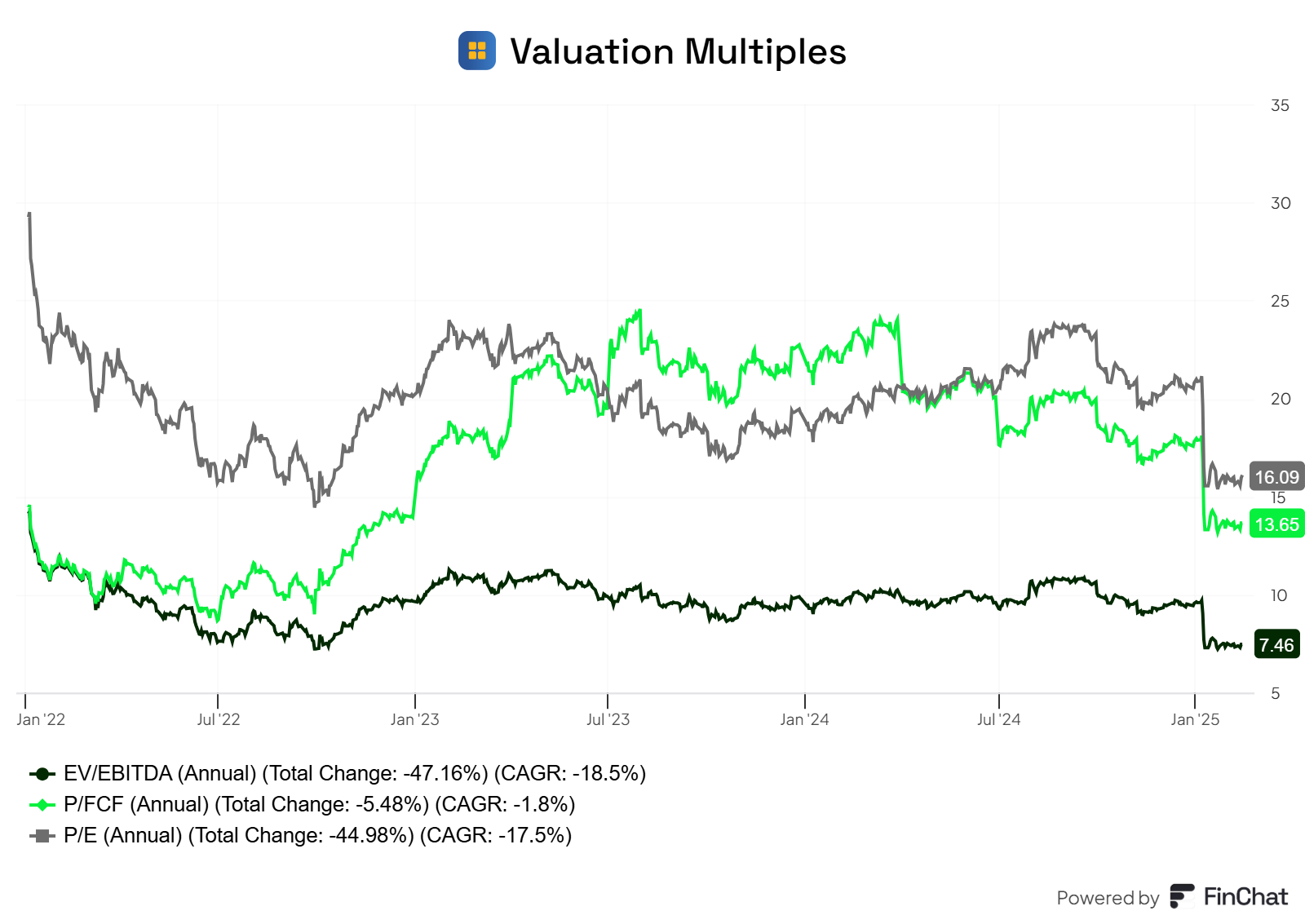

5. Valuation

Greggs is presently buying and selling at certainly one of its most tasty valuations up to now decade. With a P/FCF of 13.6x, among the many lowest ranges since 2015, it displays a compelling 7.3% FCF yield. EV/EBITDA, the one time it was decrease within the final 10 years was in 2015 at 7.4x, with at the moment’s 7.5x being the second lowest.

Over the identical interval, EBITDA has grown from £95.5M to £258.9M, reflecting an 11% CAGR, whereas FCF has expanded from £52.6M to £158.8M, a 12.3% CAGR. In the meantime, its Return on Fairness has elevated from 15.6% in 2015 to twenty-eight.7% within the first half of 2024!

Given this sturdy efficiency and Greggs’ ongoing progress technique, the present valuation seems overly conservative.

Supply: Finchat.io

6. Dangers and Alternatives

Greggs presents a combined however compelling funding case. Whereas financial headwinds persist, the corporate’s strategic variations and robust model fairness assist its long-term potential.

Funding Dangers

Financial Uncertainty: Extended inflation and weak shopper confidence might proceed to hinder gross sales progress.

Price Pressures: Rising wages, ingredient prices, and vitality bills might erode revenue margins.

Aggressive Panorama: Greggs faces growing competitors from grocery store meal offers and quick-service restaurant chains.

Funding Alternative

Resilient Enterprise Mannequin: Greggs’ value-focused proposition positions it effectively in occasions of financial uncertainty.

Enlargement Potential: Sturdy pipeline of recent retailer openings and different gross sales channels.

Digital and Supply Progress: Investments in digital ordering and supply companies present further income streams.

7. Conclusion: Is Greggs a Purchase?

Whereas short-term volatility is predicted, long-term buyers might even see worth in Greggs’ regular income progress, sturdy model, and strategic positioning. For these trying to acquire publicity to the UK shopper sector, Greggs stands out as a high-quality inventory with strong fundamentals and long-term progress potential. Let me know within the feedback should you agree!

Disclosure: I personal Greggs in my eToro portfolio.

This communication is for data and schooling functions solely and shouldn’t be taken as funding recommendation, a private suggestion, or a suggestion of, or solicitation to purchase or promote, any monetary devices. This materials has been ready with out bearing in mind any specific recipient’s funding targets or monetary scenario, and has not been ready in accordance with the authorized and regulatory necessities to advertise impartial analysis. Any references to previous or future efficiency of a monetary instrument, index or a packaged funding product will not be, and shouldn’t be taken as, a dependable indicator of future outcomes. eToro makes no illustration and assumes no legal responsibility as to the accuracy or completeness of the content material of this publication.

{kind=link}