Apple inventory has rebounded over the previous couple of months, however has lagged the Magnificent 7 leaders. The Every day Breakdown dives deep.

Earlier than we dive in, let’s be sure to’re set to obtain The Every day Breakdown every morning. To maintain getting our each day insights, all you’ll want to do is log in to your eToro account.

Deep Dive

Down over 7% to date this 12 months, Apple is the second-worst-performing Magnificent 7 element of 2025, trailing solely Tesla. Regardless of this, Apple is considered one of simply three companies with a market cap of $3 trillion or extra, sitting behind Nvidia and Microsoft.

Nonetheless, Apple has discovered some momentum these days, rallying greater than 12% over the previous three months. Is that this an indication that Apple is again — or only a bounce after a flailing begin to the 12 months?

Digging Into the Enterprise

We all know Apple because the iPhone maker — and the corporate behind Macs, AirPods, iPads, and extra. Due to its huge success, which actually dates again to the iPod and Apple Music (do not forget that?), Apple has constructed a fortress stability sheet and generates immense money move.

One downside although? Development.

Whereas Apple has loved sturdy progress over time, income and revenue progress have struggled during the last a number of years. That has compelled some buyers to search for progress in different areas — as an illustration, with shares like Amazon and Nvidia — even when meaning accepting extra volatility.

Dangers and Alternatives

Once we have a look at the valuation, Apple trades at just below 30x ahead earnings. That is costlier than the general market, however bulls argue that Apple nonetheless deserves a premium. As for whether or not it’s costly or low-cost based mostly by itself historic vary, Apple inventory sits someplace in between. Over the past 5 years, shares have usually been thought of “low-cost” at round 22x to 25x earnings and “costly” above 32x.

Traders are actually turning their consideration to Apple’s merchandise, with an iPhone refresh due within the coming months and a rising deal with AI.

AI developments had been anticipated to raise the person expertise, however delays have left each buyers and prospects questioning whether or not Apple can ship. Traders can nonetheless anticipate a gentle stream of upgrades over time — together with new iPhones, iPads, Macs, and extra — nevertheless it’s the AI element they’re most desperate to see take form.

The corporate is reportedly engaged on “an bold slate of recent gadgets, together with robots, a lifelike model of Siri, a sensible speaker with a show, and home-security cameras,” in accordance to Bloomberg.

In fact, there are dangers to this strategy — together with delays, merchandise that fail to launch, or disappointing buyer reactions. Traders should weigh Apple’s traditionally sturdy enterprise towards their expectations for future income and revenue progress.

Need to obtain these insights straight to your inbox?

Join right here

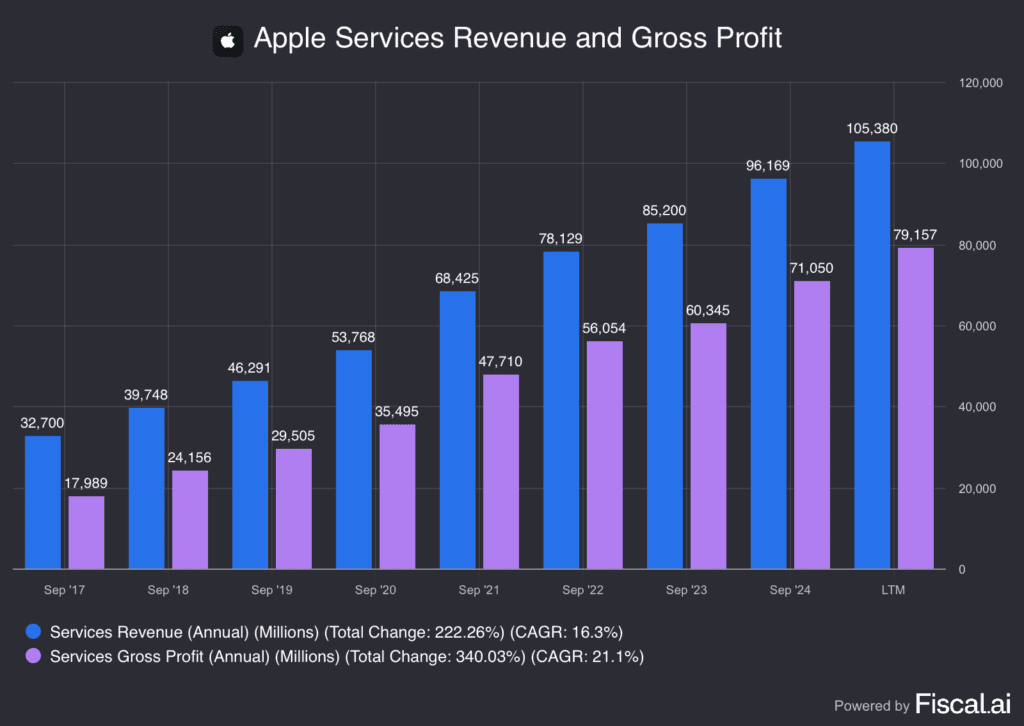

Digging Deeper — Apple’s Providers Enterprise

Apple’s {hardware} enterprise could also be trying to find new progress retailers, however its Providers enterprise — which incorporates the App Retailer, Apple Music, iCloud, Apple Pay, and extra — continues to hum alongside properly.

Income continues to develop at a strong tempo, whereas gross income — which command 75% gross margins and are greater than double the margins achieved with its Merchandise enterprise — additionally proceed to develop. So although it’s a a lot smaller income footprint, this phase makes up greater than 40% of gross revenue and continues to develop at a gentle clip.

That is one motive (of a number of) why Apple has been in a position to stay so dedicated to its huge share repurchase plan, which elevates its earnings per share — (regardless of gradual revenue progress, a shrinking share depend permits earnings per share to extend).

What Wall Avenue’s Watching

TGT

Shares of Goal are beneath stress this morning, down nearly 10% after the retailer reported earnings. The corporate beat on earnings and income estimates, however gross sales stay beneath stress. Additional, CEO Brian Cornell introduced he’s stepping down and being changed by COO Michael Fiddelke. Goal inventory pays a dividend yield north of 4.3%.

HTZ

Hertz inventory is rallying on experiences that it’s going to promote used automobiles on-line by way of a partnership with Amazon Autos. Clients who dwell inside 75 miles of 4 main cities — Dallas, Houston, Los Angeles and Seattle — will have the ability to use the brand new service. HTZ inventory is up greater than 40% 12 months to this point.

Disclaimer:

Please notice that on account of market volatility, among the costs might have already been reached and situations performed out.

{kind=link}