A bunch of Republican senators is warning US financial institution regulators {that a} little-known capital rule might successfully maintain banks out of Bitcoin, at the same time as Congress strikes to offer conventional monetary companies a bigger position in digital asset markets.

In a Could 27 letter to Federal Reserve Vice Chair for Supervision Michelle Bowman, FDIC Chair Travis Hill, and Comptroller of the Foreign money Jonathan Gould, six senators urged the businesses to construct a brand new capital framework for on-balance-sheet digital asset actions.

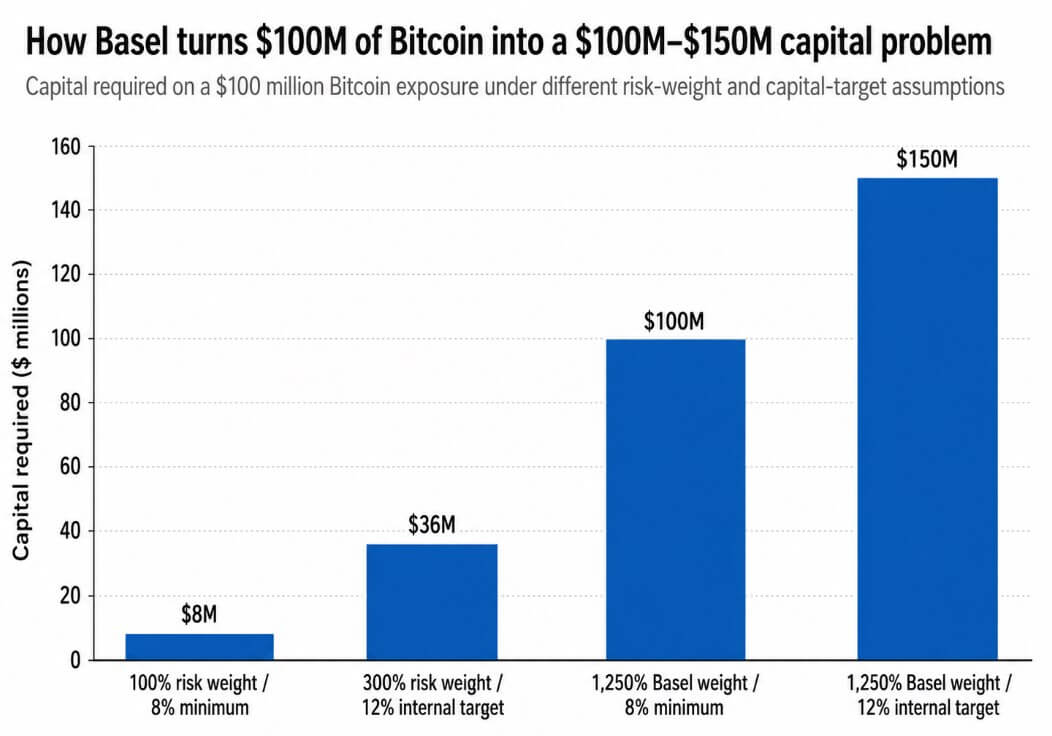

Their goal is Basel’s 1,250% danger weight for belongings similar to Bitcoin, which they argue features as a de facto ban on banks holding crypto.

A 1,250% danger weight multiplied by the 8% minimal capital requirement equals a 100% capital allocation, that means a financial institution holding $100 million in Bitcoin wants at the very least $100 million in capital towards it.

For banks that handle to satisfy inner CET1 targets above the regulatory ground, the burden climbs additional. A financial institution with a 12% inner capital goal would wish $150 million in capital for that very same $100 million publicity, requiring roughly $18 million in annual internet revenue to clear a 12% ROE hurdle.

Regular custody, buying and selling, or client-service economics hardly ever generate returns at that threshold, leaving a financial institution legally approved to carry Bitcoin however financially unable to justify doing so.

Why this lands now

The Senate Banking Committee superior the CLARITY Act on Could 14 by a 15-9 vote, sending it to the Senate ground.

If handed, the invoice would give banks a clearer statutory position in digital asset markets, however the senators argue that legislative permission with out capital effectivity leaves banks holding a permission slip they can’t afford to make use of. A financial institution could be legally approved to carry Bitcoin and nonetheless be structurally prevented from doing so by a capital cost that makes the place uneconomic earlier than the primary commerce.

The three regulators the letter addresses have every moved towards crypto permissiveness since early 2025.

The OCC reaffirmed in March 2025 that nationwide banks could have interaction in crypto custody, stablecoin-related actions, and distributed-ledger fee features, whereas eradicating the prior supervisory non-objection requirement.

The FDIC adopted that very same month, rescinding its notification requirement and permitting FDIC-supervised establishments to pursue permissible crypto actions with out prior approval.

The Fed withdrew its steering on crypto belongings and greenback tokens in April 2025, framing the transfer as assist for innovation.

All three businesses opened the door to crypto exercise and left the Bitcoin capital query untouched.The senators discovered their sharpest argumentative foothold in a March 2026 interagency FAQ on tokenized securities.

RegulatorRecent crypto-friendly moveWhat it allowed or easedWhat stays unresolvedOCCMarch 2025 guidanceCrypto custody, stablecoin exercise, DLT funds; eliminated non-objection requirementCapital remedy for bank-held BitcoinFDICMarch 2025 guidancePermissible crypto actions with out prior FDIC approvalCapital remedy for direct crypto exposureFedApril 2025 withdrawalPulled prior crypto/dollar-token guidanceCapital remedy for on-balance-sheet BitcoinFed / FDIC / OCCMarch 2026 FAQTokenized securities usually handled like underlying securitiesWhether that logic applies to native cryptoassets

The joint steering from the Fed, FDIC, and OCC held that eligible tokenized securities ought to usually obtain the identical capital remedy as their non-tokenized equivalents, and that the know-how used to document or switch possession mustn’t decide capital allocation.

If a tokenized Treasury is handled like a Treasury as a result of the underlying danger profile governs its remedy, the logic ought to prolong to Bitcoin, and the asset’s volatility and operational dangers are measurable and may assist a calibrated framework.

The March 2026 steering covers eligible tokenized securities, and the senators are urgent regulators to hold the identical technology-neutral logic ahead to native digital belongings.

The prudential case for the rule

The Fed, FDIC, and OCC’s 2023 joint assertion famous value volatility, authorized uncertainty concerning custody and possession rights, contagion from change and counterparty failures, governance weaknesses in crypto networks, and operational dangers related to open or decentralized infrastructure.

The Basel customary was constructed round these dangers after the 2022 crypto collapse uncovered how rapidly losses might unfold to interconnected establishments.

A dollar-for-dollar capital cost displays a real judgment that Bitcoin’s danger profile doesn’t resemble the belongings that populate conventional financial institution stability sheets.

The senators argue that the dangers of volatility, custody complexity, and operational publicity are quantifiable, and a calibrated capital framework can handle them with out requiring capital equal to or better than the publicity itself.

The Basel Committee agreed in November 2025 to expedite a focused overview of parts of its cryptoasset customary, and reported progress on that overview in February 2026.

Basel Chair Erik Thedéen has mentioned the worldwide crypto guidelines for banks should be reworked after the US and UK each declined to implement the present framework.

A coalition of main monetary trade teams wrote to Basel in August 2025, arguing that the usual would make significant financial institution participation uneconomical and requesting a pause and revisions.

The senators are urgent US regulators to behave at a second when the worldwide structure underpinning the 1,250% remedy is beneath open overview.

Two paths from right here

If regulators reply by proposing a calibrated framework for liquid digital belongings as a substitute of the blanket Basel weight, the capital required on $100 million of Bitcoin publicity might fall from the present $100 million-$150 million vary to one thing nearer to $8 million-$36 million beneath a 100%-300% risk-weight band and customary capital targets.

ScenarioCapital treatmentBank position in cryptoLikely market effectCalibrated framework100%-300% risk-weight band; $8M-$36M capital on $100M exposureBanks can maintain stock, assist market-making, custody, prime brokerage and structured productsMore institutional liquidity; tighter spreads; banks change into balance-sheet participantsBasel rule remains1,250% danger weight; $100M-$150M capital on $100M exposureBanks largely present custody, settlement and companies, however keep away from direct BTC exposureBitcoin entry stays routed by means of ETFs, nonbanks and offshore venues

At that stage, financial institution market-making, custody, prime brokerage, and structured crypto merchandise change into viable strains of enterprise. Institutional liquidity improves, spreads compress, and banks transfer from service suppliers to balance-sheet individuals.

If regulators maintain 1,250% remedy as the sensible customary for native crypto on-balance-sheet publicity whereas persevering with to open different pathways, banks would proceed providing custody and settlement, whereas direct Bitcoin publicity stays with nonbanks and ETF wrappers.

US-traded spot Bitcoin ETFs already noticed roughly $4.4 billion in outflows by means of Could 15 to June 3, displaying that institutional entry to Bitcoin has routed round financial institution stability sheets.

That channel will deepen if the capital rule stays intact.

The letter does elevate the political value of inaction whereas Congress is actively writing the market construction guidelines that can govern financial institution participation in digital belongings for the subsequent decade, and authorized authorization to carry Bitcoin means little if the capital cost required to take action makes the place uneconomic from the primary day it hits the stability sheet.

{kind=link}