B3 registered the primary assured OTC versatile possibility tied to Hashdex’s crypto-index ETF, HASH11, in a commerce between Inter and XP.

B3’s clearinghouse served because the central counterparty within the commerce, putting a crypto ETF-linked publicity inside the identical back-office equipment that handles counterparty threat, margining, clearing, and settlement.

That’s the infrastructure layer that Wall Avenue continues to be asking US regulators to open to tokenized property.

BlackRock submitted a response to the CFTC’s tokenized-collateral initiative in 2025, arguing that tokenized cash market funds and stablecoins must be eligible to be used in each cleared and uncleared derivatives markets.

Essentially the most concrete model of this commerce appeared offshore in April 2026, when Commonplace Chartered constructed a framework that allowed institutional OKX purchasers to submit BlackRock’s tokenized Treasury fund, BUIDL, as collateral whereas Commonplace Chartered retained custody of the property.

HASH11 served because the underlying asset of the versatile possibility, a special structural function from the margin collateral place BlackRock is asking US regulators to open to tokenized property.

Each strikes heart on how crypto-linked property enter the equipment of clearing, settlement, and threat administration.

MarketDevelopmentAsset roleInfrastructure layerWhy it mattersBrazil / B3Guaranteed OTC versatile possibility tied to HASH11Underlying assetCCP, margining, clearing, settlementCrypto ETF-linked publicity enters regulated derivatives plumbingU.S. / BlackRockTokenized cash market funds and stablecoins in derivatives marketsCollateral / marginCleared and uncleared derivatives collateral systemsWall Avenue desires tokenized property accepted in risk-management workflowsOffshore exampleStandard Chartered / OKX / BUIDL collateral frameworkPosted collateralCustody + institutional collateral managementShows the tokenized collateral mannequin rising outdoors U.S. rulemaking

The HASH11 versatile possibility is customizable by maturity, strike, amount, premium, and non-obligatory options similar to limitations or limiters.

On Might 6, B3 started accepting actual property funding funds as eligible collateral for CCP-guaranteed operations, bringing the eligible pool to roughly $146 billion. B3’s collateral checklist already consists of Brazilian exchange-traded ETF quotas below normal eligibility standards.

Each selections to broaden eligible collateral and introduce HASH11 as a by-product underlier display how B3 is broadening the asset sorts that enter its regulated clearing and settlement framework.

Why Brazil earned this second

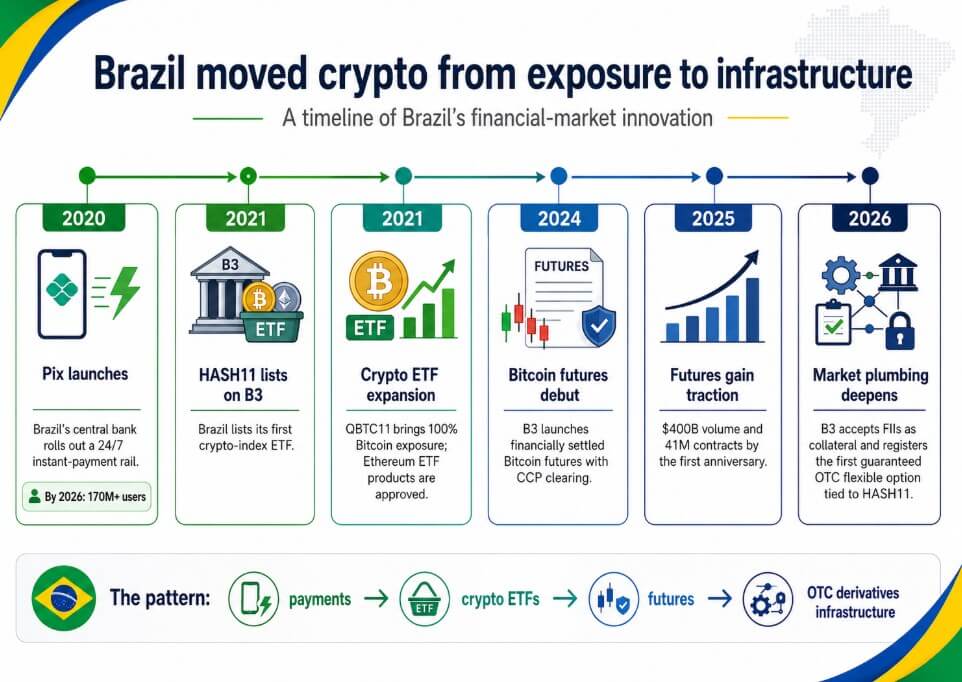

Brazil’s capacity to execute this commerce rests on a monetary system that has repeatedly adopted infrastructure-level improvements earlier than bigger markets completed debating them, with the clearest instance being Pix.

Brazil’s central financial institution launched the 24/7 instant-payment rail in 2020, and by 2024, Pix had processed greater than $5 trillion and surpassed money, debit playing cards, and bank cards as Brazil’s main fee technique.

By 2026, the community had reached greater than 170 million customers throughout round 900 taking part establishments, and Banco do Brasil had begun enabling Pix funds in Argentina.

The crypto ETF file adopted the identical arc, as Hashdex launched what Nasdaq described because the world’s first crypto ETF on the Bermuda Inventory Alternate in February 2021, and B3 listed HASH11 in April 2021 as Brazil’s first crypto-index ETF.

QBTC11 started buying and selling on B3 in June 2021 because the change’s first ETF with 100% Bitcoin publicity. QR Asset marketed QSOL11 because the world’s first spot Solana ETF, and Brazil authorized Ethereum ETF merchandise in 2021, years earlier than US spot Ethereum ETFs turned normal market infrastructure.

Bitcoin futures debuted on B3 in April 2024 with monetary settlement, and the inventory change acted because the CCP. By the primary anniversary, $400 billion in buying and selling quantity and 41 million contracts had established the product as a functioning hedging market, with non-resident buyers accounting for 53% of participation, people for 39%, and funds for 7%.

What Wall Avenue sees on this

Collateral, clearing, margin, and settlement are the techniques that permit establishments hedge, lever and handle threat at scale, representing crypto adoption’s subsequent part.

That’s precisely the infrastructure layer BlackRock is working to modernize in Washington, and it’s precisely the place Brazil has been constructing for 4 years.

When BlackRock argues that tokenized property ought to enter derivatives collateral techniques, the declare is that crypto-linked monetary merchandise are mature sufficient to function inside risk-management infrastructure, and Brazil’s file helps that empirically.

B3 has a CCP, margining and settlement frameworks, crypto futures with $400 billion in quantity, and now a assured OTC versatile possibility tied to a crypto ETF inside the identical clearinghouse stack.

Brazil’s innovation stack, consisting of Pix for funds, B3 for listed and OTC market infrastructure, crypto ETFs for regulated publicity, and Bitcoin futures for hedging, operates as a coherent entire moderately than remoted bets.

How far the plumbing extends

Within the bull case, B3’s infrastructure stack turns into a reference mannequin for a way crypto-linked property can graduate into regulated clearing equipment, extra crypto underliers enter OTC versatile choices, and the collateral menu broadens.

A measurable threshold, similar to crypto-linked OTC notional reaching 1% to five% of B3’s assured flexible-options inventory throughout the subsequent 12 to 24 months, would affirm the HASH11 possibility has moved from a one-off institutional commerce right into a functioning market phase.

ScenarioWhat occurs nextSignal to watchArticle implicationBull caseMore crypto underliers enter OTC versatile choices; collateral menu broadensCrypto-linked OTC notional reaches 1%–5% of B3’s assured flexible-options stockBrazil turns into a reference mannequin for regulated crypto derivatives plumbingBase caseHASH11 choices repeat, however stay institution-focusedA handful of latest trades, largely bespokeBrazil is forward, however adoption is gradualBear caseLiquidity, volatility and margin constraints restrict expansionCollateral pool stays dominated by Selic federal debtCrypto stays largely in wrappers, not core market plumbingBlack-swan caseMarket shock or regulatory warning triggers tighter eligibilityHigher haircuts, fewer eligible merchandise, slower approvalsCrypto infrastructure narrative stalls

Within the bear case, B3’s $146 billion collateral pool was greater than 82% Selic federal debt as of Might 2026, and crypto-linked publicity carries liquidity and volatility traits that work towards it within the core collateral stack, the place margin necessities and haircuts are the binding constraint.

If regulatory warning tightens eligibility or liquidity proves skinny, the HASH11 OTC possibility stays a bespoke institutional product, and crypto stays in funding wrappers.

Brazil laid the groundwork for this infrastructure race, enabling monetary improvements to maneuver rapidly from experiment to functioning market infrastructure, whereas BlackRock continues to be making its regulatory case in Washington.

The gap between the place Wall Avenue desires to go and the place Brazil already is retains widening.

Price Prediction 2026 2027 2028")

Bounce Under Threat As Resistance Caps Further Gains")

{kind=link}