Rethinking CEX Listings, Onchain Liquidity, and What “Market Making” Actually Means

For years, the default path was easy: launch a token, chase centralized alternate listings, rent a market maker (or don’t), hope all of it works out. That path nonetheless exists however is it aligned with what token tasks truly want?

Ought to token tasks be their very own onchain market maker?

It’s a query that has been making its approach into an increasing number of conversations, so I invited Primal Glenn (BD at Bancor) and Dr. Mark Richardson (Venture Lead at Bancor) to affix me on a Blockchain Banter devoted to the subject.

We walked by means of an actual instance, full with what makes it tough for tasks to make a market on conventional and concentrated liquidity AMMs, and explored what a greater, clear onchain setup can look like.

The CEX itemizing drawback nobody desires to speak about

Glenn opened with a concrete case.

A brand new mission — no token reside but, however with a token central to its protocol — was just lately getting ready for its TGE (token technology occasion). As a part of the launch, they approached centralized exchanges.

What they had been instructed by one specifically is one thing many founders have quietly heard:

The alternate wished 8–10% of the full token provide.On high of that, there have been itemizing charges.And past that exist anticipated market-making preparations — both direct retainers or token loans to third-party market makers.https://medium.com/media/21891816a66d2310843edf00981de492/href

“From day one, that’s an enormous chunk of provide and capital out the door.” And this isn’t nearly getting an inventory; it’s about funding ongoing market high quality on these venues.

Mark added nuance: in lots of “conventional” setups, it’s normally the market maker — not the alternate — that receives a big token allocation, underneath a contract that aligns incentives and defines how these tokens might be used.

In crypto, the traces are blurry:

Many centralized exchanges successfully act as each the venue and the dominant market maker.Some ask for token allocations which might be then distributed to their very own token holders by way of launchpads, quests, or staking packages.Tasks can discover themselves paying charges and handing over provide for packages that principally profit the alternate’s personal ecosystem, not their very own respective group.

Mark summarized it bluntly: a few of these offers are “par for the course, however possibly somewhat extra predatory than impartial.”

On this specific case, the mission determined to stroll away, although not with out exposing the supposed predatory techniques of the centralized alternate first.

https://medium.com/media/43aecd8acfd59fe2d76a2d6df8437e41/href

Onchain launches and the transparency entice

The mission selected to skip the CEX route and conduct its TGE onchain utilizing an ordinary fixed product AMM. On paper, that sounds extra clear and truthful.

In follow, it raised a special drawback.

Onchain observers watched because the mission was promoting into the pool, a unilateral promote strain.

The Crypto Twitter group was fast to reply, saying that in the event that they had been making an attempt to “market make,” — like they claimed — customers count on to see:

Each promoting and shopping for, not simply promoting.Some type of seen construction to the technique.

The mission might need had a plan however the mechanics weren’t apparent. And with out a clear clarification, it appeared as if the workforce was merely dumping on the market.

If tasks do need to be their very own market maker onchain, what instruments do they really have and the way can the mechanics be apparent to onlookers?

Why conventional AMMs don’t match what tasks want

To grasp the constraints, Mark went again to fundamentals.

The earliest Bancor swimming pools used the traditional fixed product AMM:

If a mission desires to seed a pool with, say, $50,000 value of its token and $50,000 of USDC, it appears respectable. Market cap might be inferred, the pool appears deep, and a market exists.

However at launch, nearly nobody exterior the mission holds the token.

Which means:

If nobody holds the token but, nobody can promote into the pool.The preliminary USDC is essentially symbolic — successfully untouchable till somebody buys the token.

On high of that, the mission is compelled to lock up significant quantities of quote belongings (USDC, ETH, and so on.) in a construction that doesn’t replicate how a mission truly thinks about its token:

It desires to promote a token provide at chosen costs, not simply “from 0 to infinity.”It desires to transparently purchase again at a lower cost, not the place it simply offered.It desires to fund operations and handle runway utilizing these proceeds.

Fixed product AMMs weren’t designed with this use case in thoughts. They had been designed to create steady, permissionless liquidity — to not successfully, strategically make a market.

https://medium.com/media/50c2215a18f228d73ab7910dfc85c1df/href

Concentrated liquidity: extra management, nonetheless the fallacious form

Amplified liquidity, generally generally known as concentrated liquidity, was meant to repair a few of these inefficiencies.

Glenn identified that with concentrated liquidity:

A mission can present single-sided liquidity out of the cash (for instance, solely its personal token at a better worth than the present market).It could actually determine, “I need to promote from this worth upward, with out having to seed each belongings.”

That’s a step nearer to what a token issuer would possibly need.

However Mark highlighted a elementary constraint: concentrated liquidity techniques nonetheless observe the identical underlying rule:

When your asks are taken, they’re transformed into bids behind the worth you simply traded at, minus a “charge”. I put this in citation marks as a result of Mark despises the time period “charge” in DeFi. For extra on that although, see his EthCC presentation “Fixing Objectively Unhealthy Fashions in LP Efficiency Evaluations”

Fixing Objectively Unhealthy Fashions in LP Efficiency Evaluations | EthCC[9] Archives

Put in a different way:

If a pool sells a token at a given worth, it then mechanically affords to purchase it again at practically the identical worth.That may be wonderful for consumer-focused liquidity, however it’s not how a mission or skilled market maker sometimes manages danger.You may promote hundreds of thousands value of tokens, solely to be compelled to face prepared to purchase all of them again at nearly the identical worth, for a tiny charge.

To make this behave extra like an actual market-making engine, you’d want:

Automation to withdraw liquidity on the proper time.Bots (keepers) to repost liquidity at new costs.A continuing battle for blockspace and fuel in opposition to different onchain actors.Further third-party infrastructure and related charges.

Glenn summed it up: in the event you attempt to run a real purchase low, promote excessive technique throughout a number of worth ranges utilizing normal CLAMMs, you find yourself with an advanced, fragile bot stack, and also you’re nonetheless constrained by the protocol’s construction.

https://medium.com/media/4f9b2d36ef32cd8b1aeeb2281369af4b/href

What tasks really need from onchain market making

From the founder’s perspective, the want listing is easy:

Promote tokens at outlined worth factors or over an outlined worth vary.Purchase again tokens at decrease costs utilizing proceeds, in a approach that may run with out bots or babysitting blocks.Preserve every part onchain and clear, so the group can see the logic and construction.Keep away from opaque off-exchange offers, double-dipping itemizing phrases, and misaligned incentives.

In different phrases:

“Let the mission categorical its meant market construction straight onchain — without having to wire half its provide to an alternate or keep a fragile net of bots.”

That’s the place Carbon DeFi entered the dialog.

How Carbon DeFi turns token tasks into onchain market makers

Glenn walked by means of how Carbon DeFi is being utilized by token tasks at present to construct precisely the type of construction this specific mission was lacking.

At a excessive degree, Carbon DeFi lets a token mission:

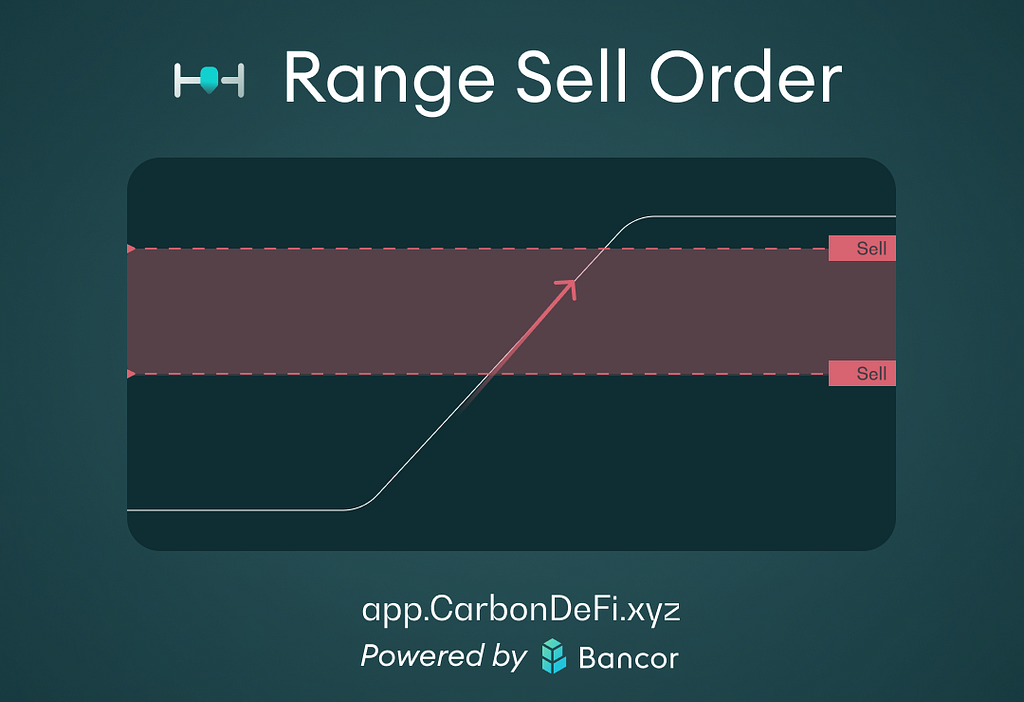

1. Outline a promote order

Single-sided if desired (for instance, solely the mission’s token).Both at a selected worth or throughout a spread (e.g., promote from $0.37 as much as $0.50).All onchain, seen to anybody.

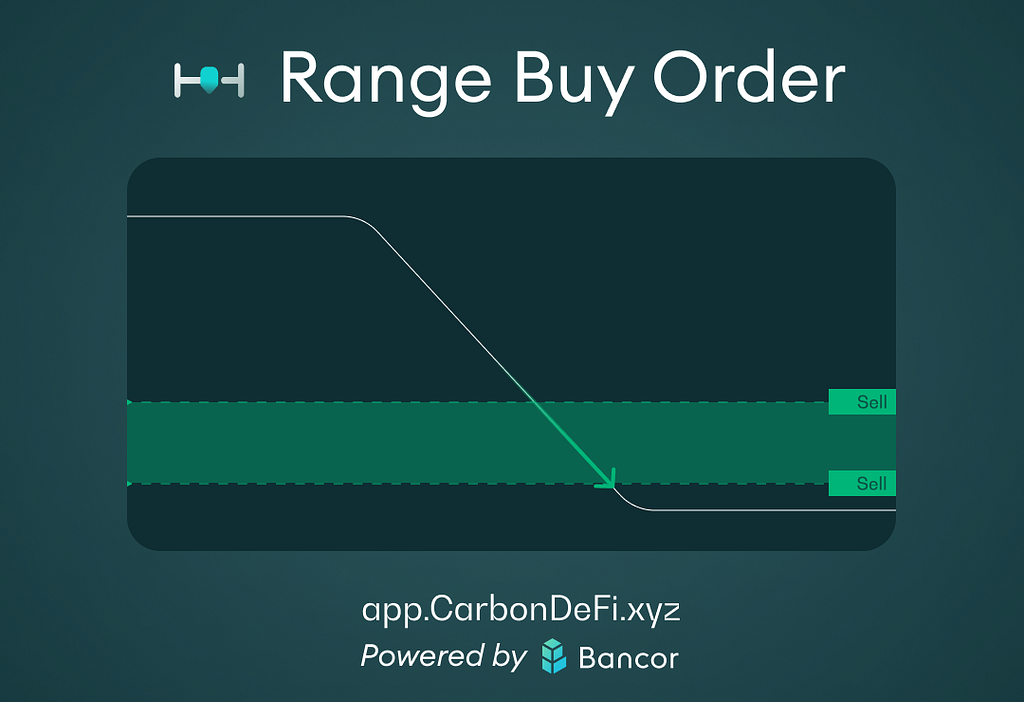

2. Outline a purchase order at a special worth

Purchase again the token at a lower cost or vary utilizing the proceeds from the promote order.This purchase order is linked to the promote order, however not constrained to the identical worth degree like a typical CLAMM.

3. Recycle proceeds mechanically

When the promote aspect executes, the token acquired is mechanically rotated into the purchase order.When the purchase aspect executes, the bought tokens rotate again to the promote aspect.The result’s a recurring, “purchase low, promote excessive, repeat” loop, solely onchain.

Crucially:

The mission can fund just one aspect initially (for instance, simply its personal token) and let proceeds fund the opposite aspect.It could actually modify ranges, costs, funding, and technique sort at any time with out tearing down and rebuilding every part.Each technique is absolutely clear:Orders reside onchain.The Carbon DeFi UI can show methods, fills, edits, and timestamps.Tasks can share direct technique hyperlinks with their communities.

This addresses precisely the criticisms that hit the mission in Glenn’s instance:

As an alternative of a pockets that “simply sells,” viewers can see a structured promote vary and a corresponding purchase vary.As an alternative of making an attempt to deduce intent from random transactions, customers can see the meant market logic encoded as a method.

As Glenn put it, this isn’t about outsourcing every part to an exterior market maker; it’s about giving token tasks a local, protocol-level method to construction their very own markets onchain — with out bots, keepers, or offchain contracts.

So, ought to token tasks be their very own onchain market maker?

By the tip of the dialog, the reply wasn’t a easy sure or no.

On centralized exchanges, “being your personal market maker” is commonly unrealistic. The platform, the itemizing phrases, and the market-making relationships are tightly coupled, and small tasks are not often in management.

Onchain, it’s totally different.

If a token mission:

Controls its provide,Has a transparent concept of the way it desires to distribute and recycle that offer, andUses tooling that lets it categorical actual market logic straight onchain,

then sure — being its personal onchain market maker can’t solely be viable, however preferable.

As Mark famous:

A mission that controls its personal token provide will not be sure by the identical constraints as a third-party market maker that has to function purely for revenue. It could actually outline success in a different way: distribution, stability, runway, group alignment.

What issues is having infrastructure that respects that actuality. For a lot of groups, that’s beginning to look much less like a centralized itemizing negotiation — and extra like constructing clear, programmable onchain markets with techniques like Carbon DeFi.

Full Recording

https://medium.com/media/d6d220a6d49b951a3ed0101c420804df/href

Blockchain Banter

Blockchain Banter is a reside, unscripted dialogue sequence the place trade consultants, builders, and thought leaders come collectively to share data, problem concepts, and discover the evolving panorama of DeFi and blockchain.

🎙️ Comply with me on X at x.com/Here2DeFi and tune in weekly on Wednesdays at 3PM UTC.

Offered by Bancor

Bancor has all the time been on the forefront of DeFi innovation, starting in 2016 with the invention of the Fixed Product Automated Market Maker and “pool tokens” — which nonetheless stay extensively used throughout the trade. The most recent innovations powering Carbon DeFi and Arb Quick Lane substantiate Bancor’s deep dedication to delivering excellence, advancing the trade, and pushing the boundaries of what’s attainable on the planet of decentralized finance. For extra info, please go to www.bancor.community.

Ought to Token Tasks Be Their Personal Market Maker? was initially printed in Bancor on Medium, the place individuals are persevering with the dialog by highlighting and responding to this story.

{kind=link}